- Authors

- Marion Vieweg, Naville Geiriseb, Linda Caceres Leal (Agora Verkehrswende)

- Publication number

- 143-2026-EN

- Version number

- 1.0

- Publication date

-

26 March 2026

- Pages

- 58

- Suggested citation

- Agora Verkehrswende and GIZ (2026): Towards Decarbonising Transport 2026 – A Stocktake on Sectoral Ambition in the G20.

Towards Decarbonising Transport 2026

A Stocktake on Sectoral Ambition in the G20

Preface

Ten years have passed since the Paris Agreement was adopted and signatory nations made their first round of national commitments. The transport sector, which is responsible for moving people and goods by road, rail, air or waterway, is essential for economic development, international trade and social participation. In recent years, the importance of decarbonising the transport sector has gained considerable attention, with several international initiatives, such as the ZEV Transition Council and the Transport Decarbonisation Alliance, working towards this goal. These are welcome developments. However, fossil fuels remain dominant and, while growth in transport emissions has slowed, it has not yet peaked. Furthermore, recent international conferences have failed to generate stronger political momentum for transformation.

This publication analyses the current state of decarbonisation and climate ambition in the transport sectors of G20 countries. The document is an update of the report “Towards Decarbonising Transport 2023 – A Stocktake on Sectoral Ambition in the G20”. The current report is the latest in a series that started with the first publication in 2017. This enables analysis of developments since the initial publication.

The report summarises the transport sector mitigation policies enacted by G20 countries and describes their progress in decarbonising the sector up to 2024. The focus is on G20 countries because, collectively, they account for just under 80 percent of global economic output and two thirds of current global CO₂ emissions, as well as 60 percent of the world’s population. Despite international efforts to limit global warming to well below 2°C, transport emissions are still growing, which is why the G20’s decarbonisation efforts are so crucial.

By including the African Union in the G20, the group now also represents a rapidly growing continent. Furthermore, G20 leaders met on African soil for the first time under South Africa’s presidency in 2025. By 2050, it is projected that a quarter of the world’s population will live in Africa, compared to 15 percent today. Coupled with rising incomes and an expanding middle class, emissions are set to rise substantially. As transport sector emissions are growing much more rapidly than those in other sectors, leapfrogging to low-carbon alternatives in Africa would provide substantial climate benefits as well as development opportunities. This publication examines where Africa is today in terms of decarbonising the transport sector, and the associated challenges and opportunities.

This report provides an overview of the G20 countries’ ambitions in this sector to date. For the first time, it is accompanied by an interactive online dashboard providing the latest comprehensive data on transport, energy and mobility, as well as the current status and development of transport sector commitments and policies. We hope that this report will contribute to a vibrant policy dialogue in subsequent years, because the success of the transformation will depend crucially on evidence-based international exchange.

1 | Is the G20 making progress?

Ten years have passed since the landmark adoption of the Paris Agreement in 2015. Many countries have updated their nationally determined contributions (NDCs) since the initial submissions in 2015, increasing their ambition over time. However, by mid-January 2026, only 110 Parties had submitted their third round NDCs, representing 136 countries, including 18 of the original G20 members,1 while 188 countries had submitted initial NDCs in 2015 and 2016. This demonstrates a lack of urgency among many countries. Similarly, COP30 ended without a clear signal for the required phase-out of fossil fuels. As the world’s largest economies, G20 countries are uniquely suited to play a leading role in enabling and driving the decarbonisation of the transport sector. Additionally, in 2023, the African Union joined the G20, representing all African countries. These developments warrant closer examination of the G20’s role in decarbonising the transport sector. This report will address the following questions:

- Can we see progress since 2015?

- Is there a clear link between current policies and observed trends?

- What is Africa’s role in decarbonising transport?

1.1 The role of G20 members in the face of shifting global dynamics

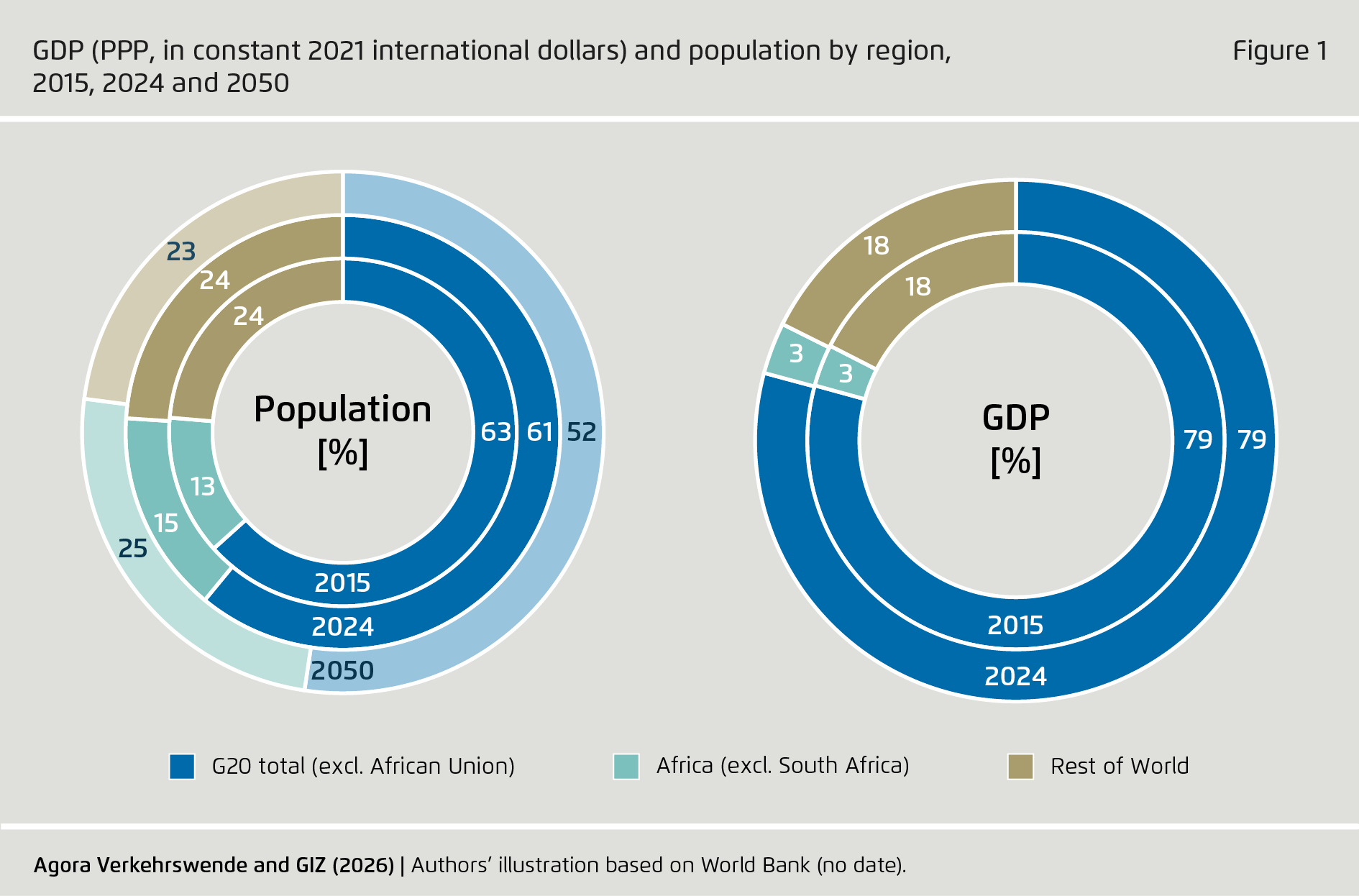

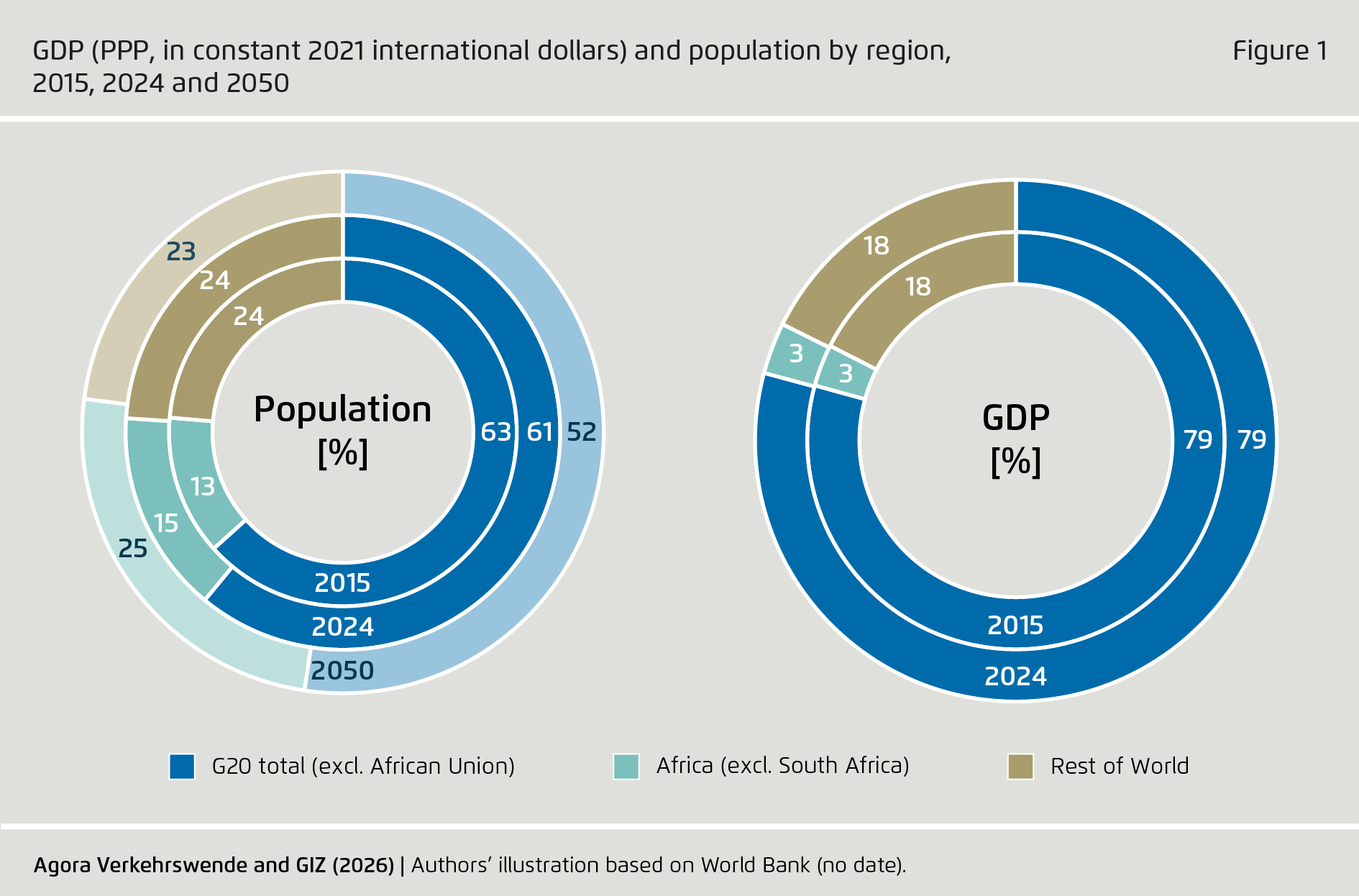

Over the past decade, the G20 has maintained strong economic development and has remained a major actor in the domain of climate policy. Between 2015 and 2024, the G20’s share of global GDP remained almost constant at just under 80 % (see Figure 1). Over the same period, global GDP increased by 31 %. Africa remains a minor economic player, generating only 3 % of global GDP in 2024 (when South Africa is excluded).

The global population grew by 9 % between 2015 and 2024, increasing from 7.44 billion to 8.15 billion people. The UN projects that this figure will increase by a further 19 % by 2050, reaching 9.66 billion. Most of this growth is expected to occur outside of the G20 countries. Over the past decade, the G20’s share of global population decreased from 63 % to 61 %. Over the same time period, Africa (excluding South Africa) increased its population share from 13 % to 15 %, and it is expected to be home to a quarter of the world’s population by 2050. Together with the original G20 countries, the extended G20 would represent 77 % of the global population by 2050.

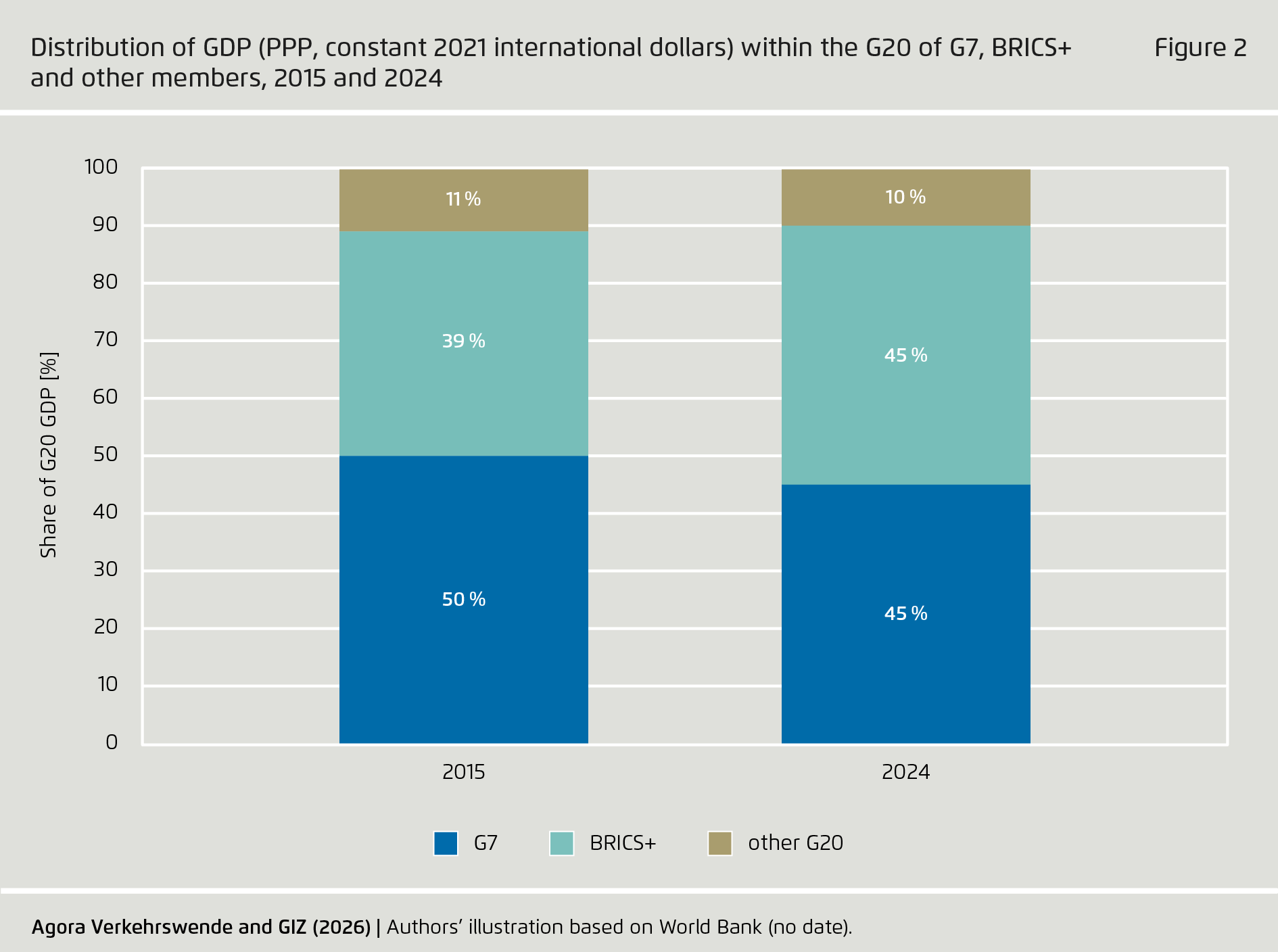

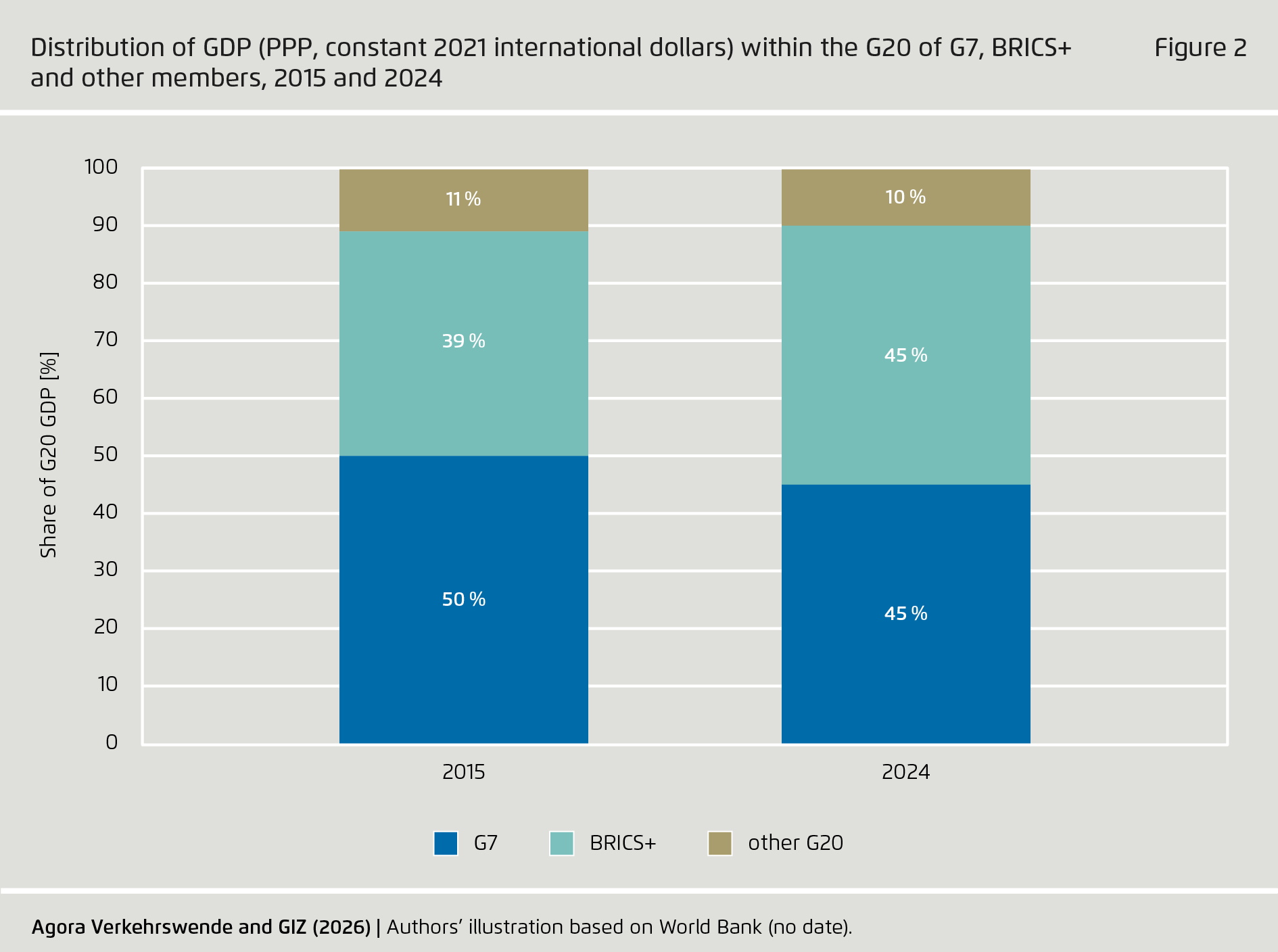

In addition to changes in the relevance of the G20 at the global level, shifts are also occurring within the group itself. In 2015, the G7 (comprising Canada, France, Germany, Italy, Japan, the United Kingdom and the United States) were responsible for half of the group’s GDP. A decade later, the group represented 45 % of the G20’s GDP – a five percentage point drop, despite collective GDP growth of 18 % (see Figure 2). During this period, the BRICS+ group (consisting of Brazil, China, Russia, India, Indonesia and South Africa) increased their GDP by 51 %, raising their GDP share in the G20 from 40 % to 45 %. Growth within the BRICS+ group is mainly driven by growth in China and Indonesia.

1.2 Slower growth in transport emissions

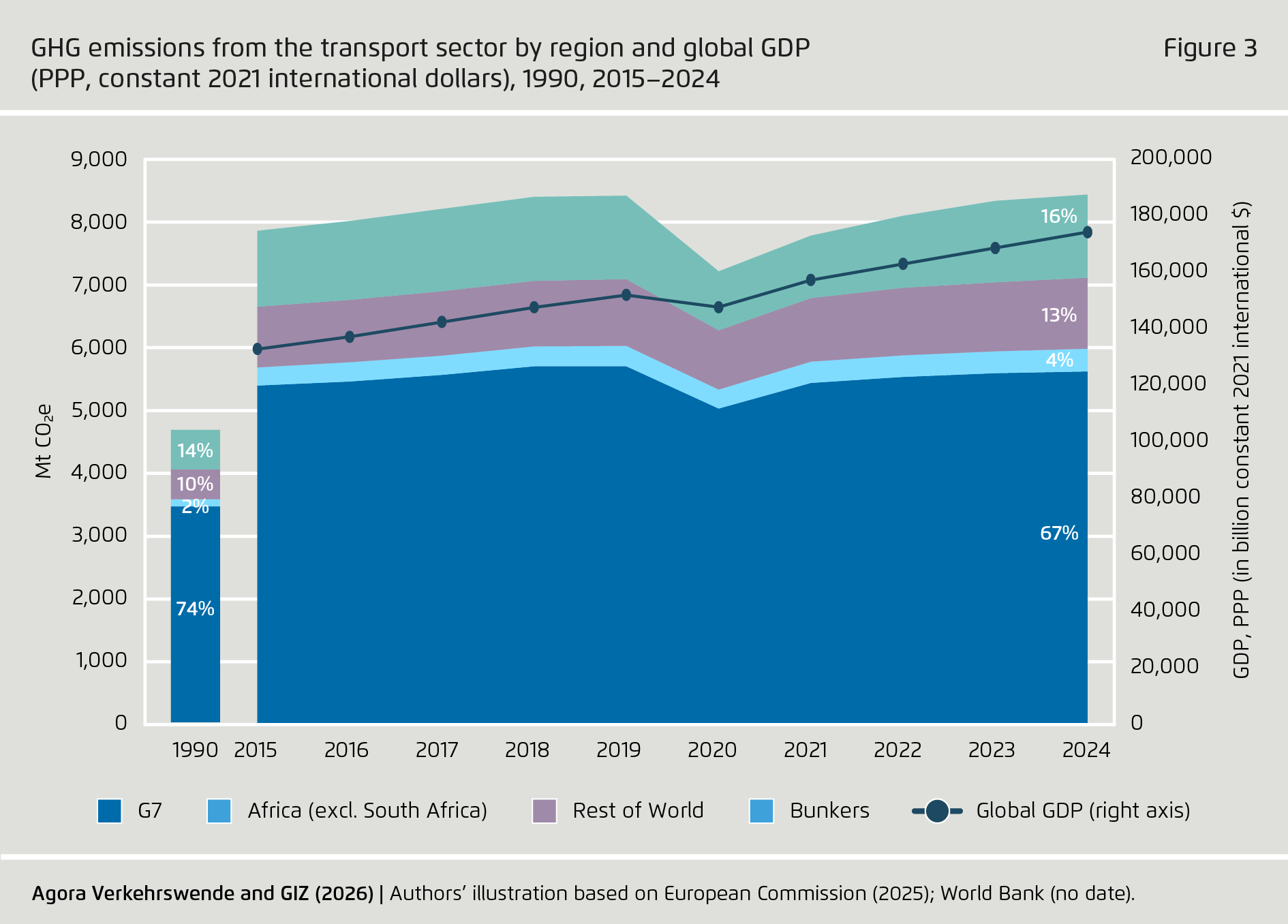

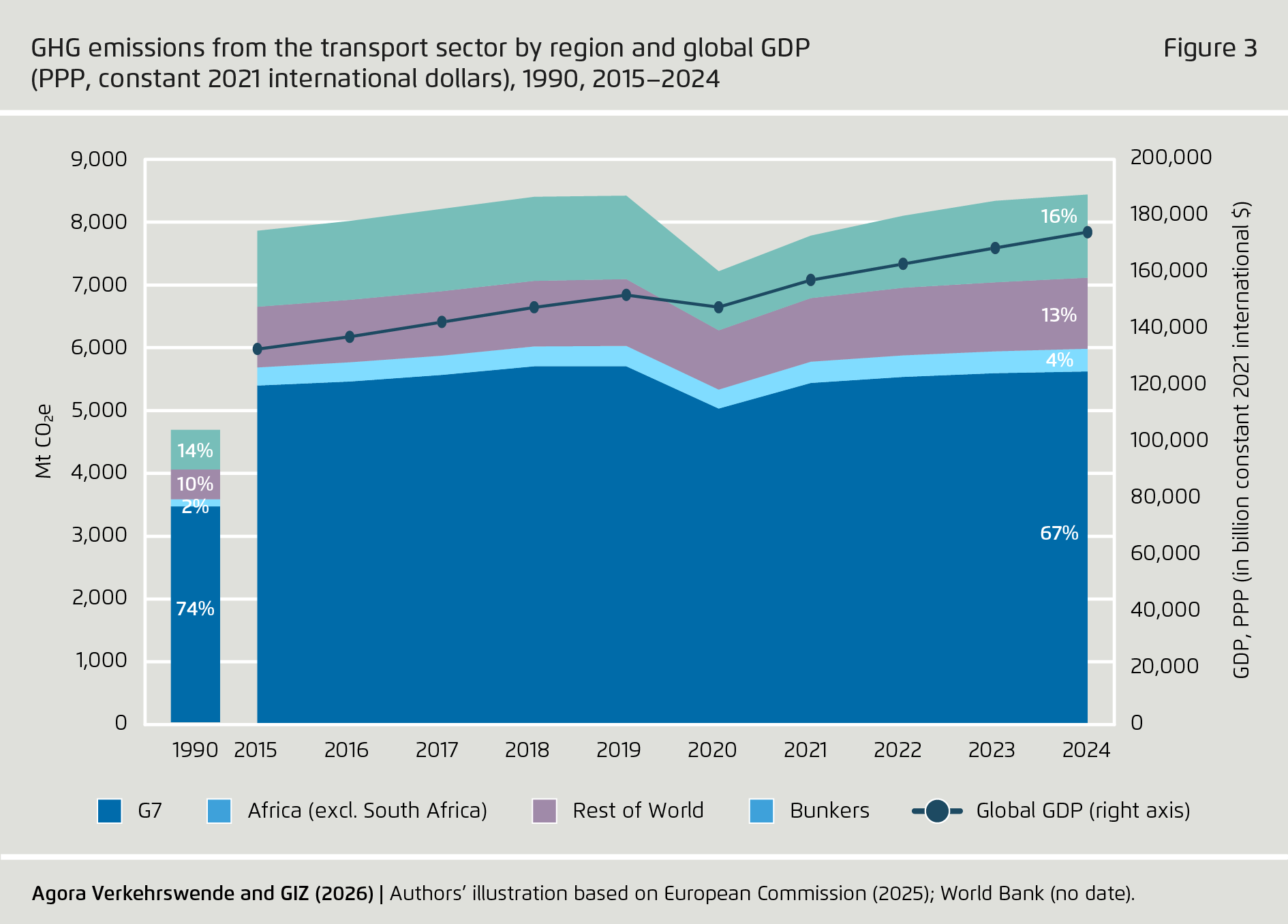

Global greenhouse gas emissions from transport dropped significantly during the pandemic, but started to increase again in 2021. By 2024, emissions had reached pre-pandemic levels, although growth slowed down that year. Compared to 2015, global emissions from the sector have increased by 7 %, which is much lower than in previous decades, which saw growth rates of 26 % (1995–2004) and 15 % (2005–2014).

Global GDP increased by 31 % between 2015 and 2024, growing much faster than emissions from the transport sector. This indicates a slow decoupling of economic development from transport emissions, even if some of the slowdown in emissions growth is likely attributable to the pandemic (see Figure 3).

Transport emissions in the G20 countries increased by 4 % over the past decade, with growth remaining below global levels. Consequently, the group’s share of global emissions in transport has fallen slightly, from 69 % to 67 %. Nevertheless, compared to 1990, when the G20 were responsible for nearly three-quarters of global transport emissions, the decline is substantial.

Transport emissions in Africa (excluding South Africa) have increased the most, experiencing a 26 % rise between 2015 and 2024, although from very low starting levels. Over the past decades, transport emissions in Africa and the rest of the world (excluding the G20) have seen a disproportionate increase, rising from 12 % to 17 % between 1990 and 2024.

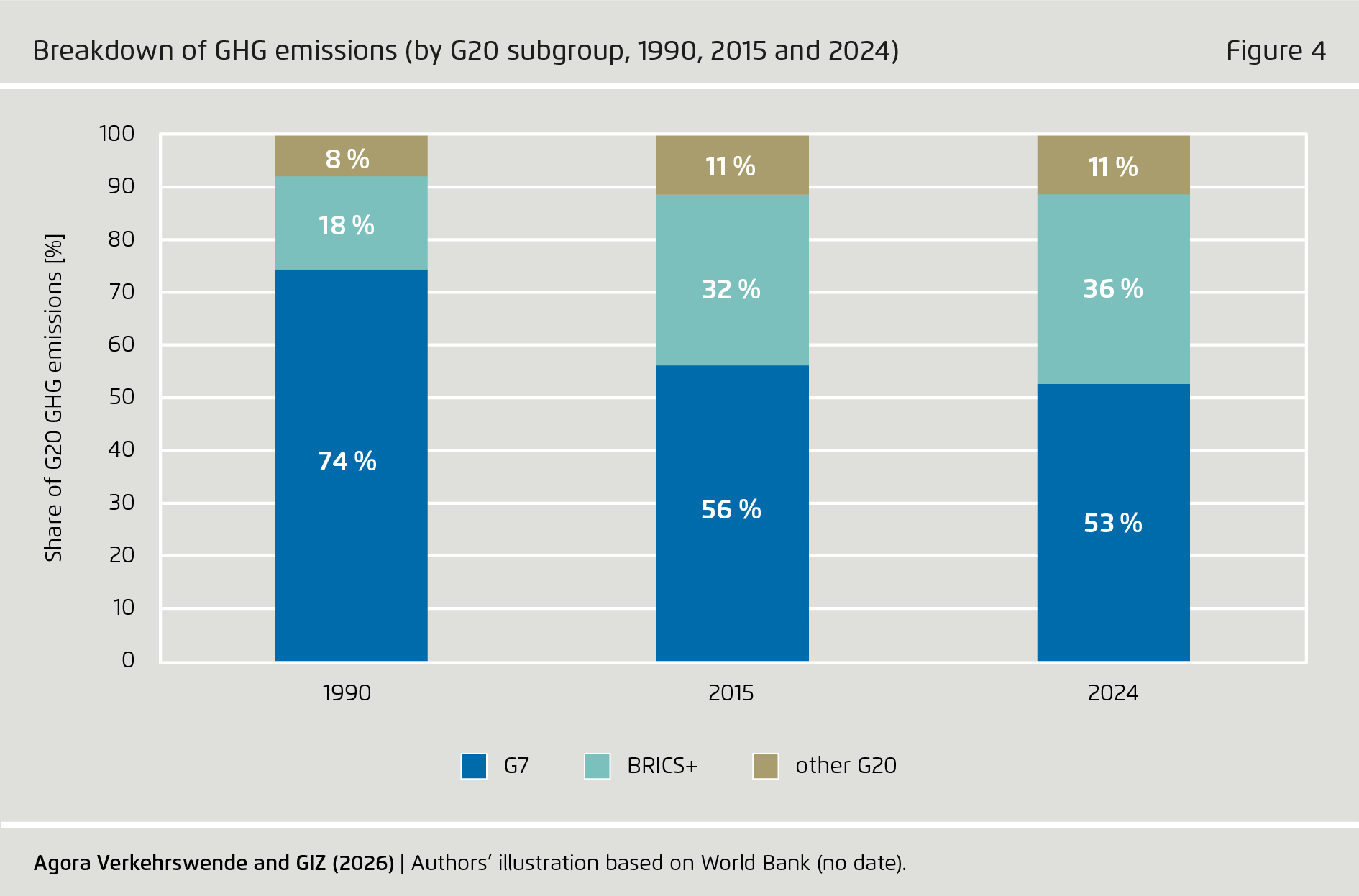

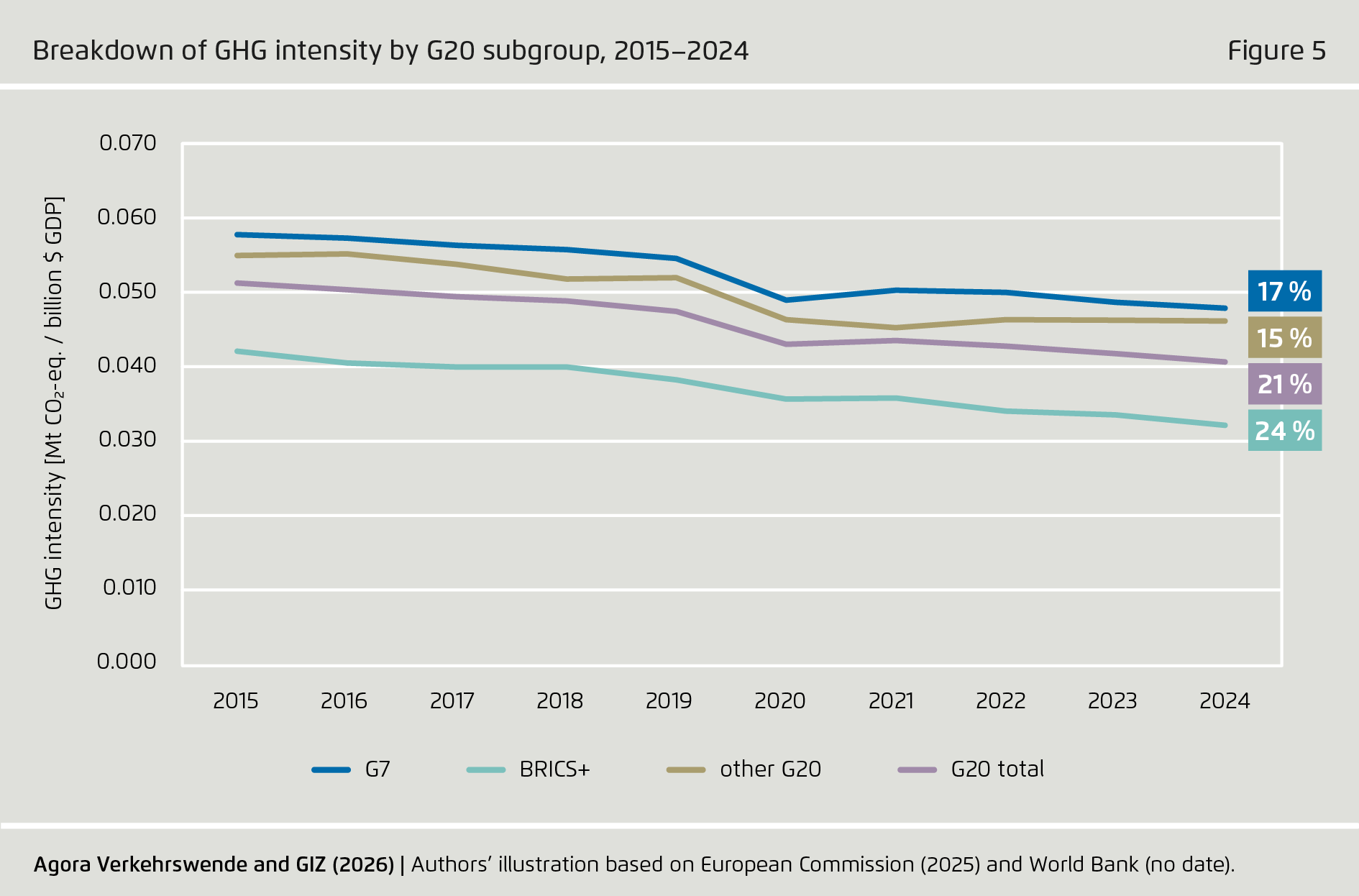

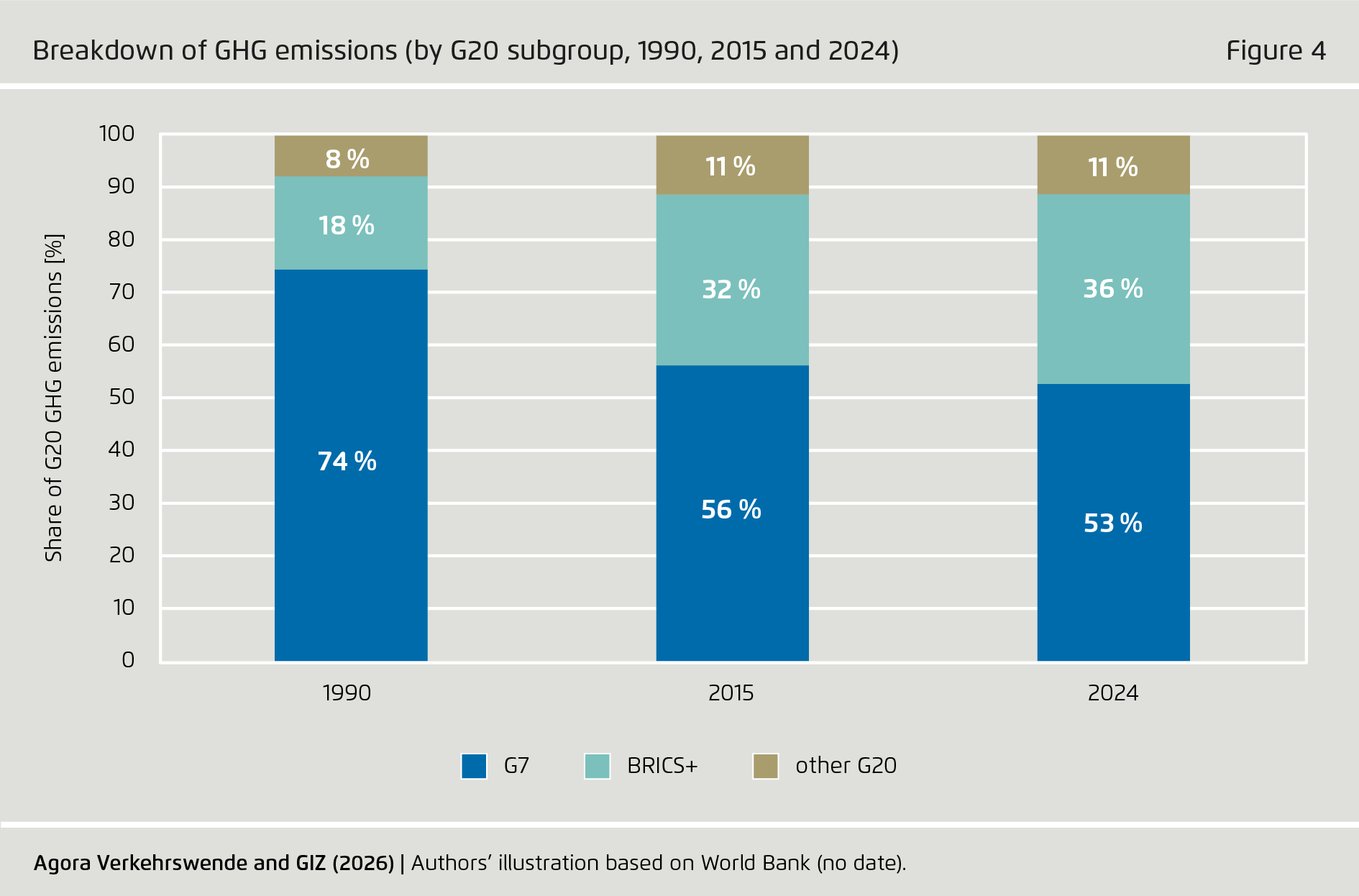

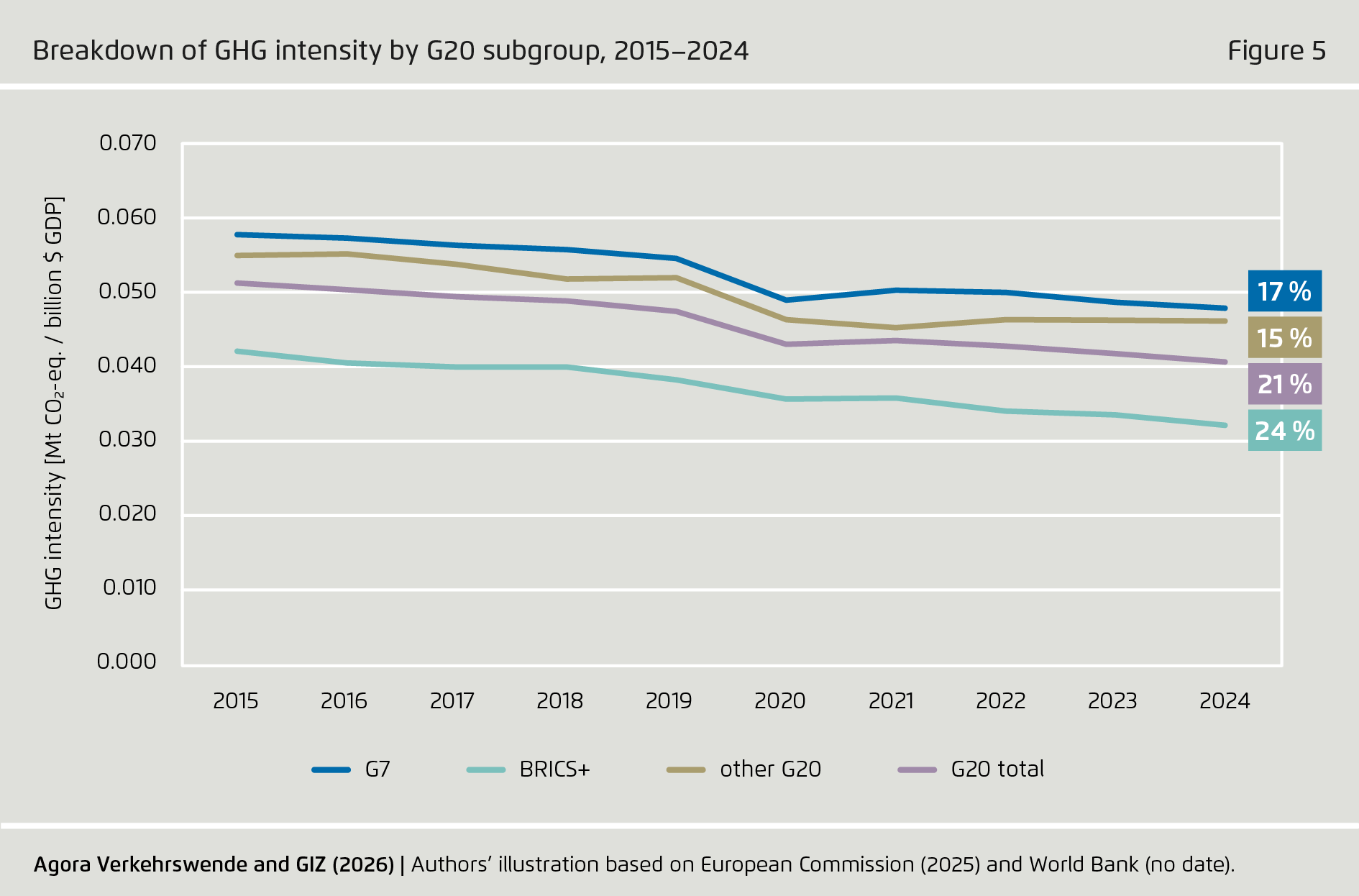

While transport sector emissions in the G20 have remained almost stable over the last decade, their source has shifted. In 1990, the G7 were responsible for 74 % of emissions from the group. This share fell to 56 % by 2015, and declined even further, to 53 %, by 2024. Conversely, the BRICS+ group has increased its share of emissions, accounting for more than a third of the G20’s emissions in 2024 (see Figure 4). Nevertheless, GDP has been growing faster than emissions, leading to a decrease in the emissions intensity of GDP. This is true of all G20 subgroups, but BRICS+ members of the G20 are decoupling emissions from GDP growth faster than others, while also starting from lower initial levels (see Figure 5).

1.3 Vehicle electrification is expanding in all G20 countries, with low-carbon power generation growing even faster

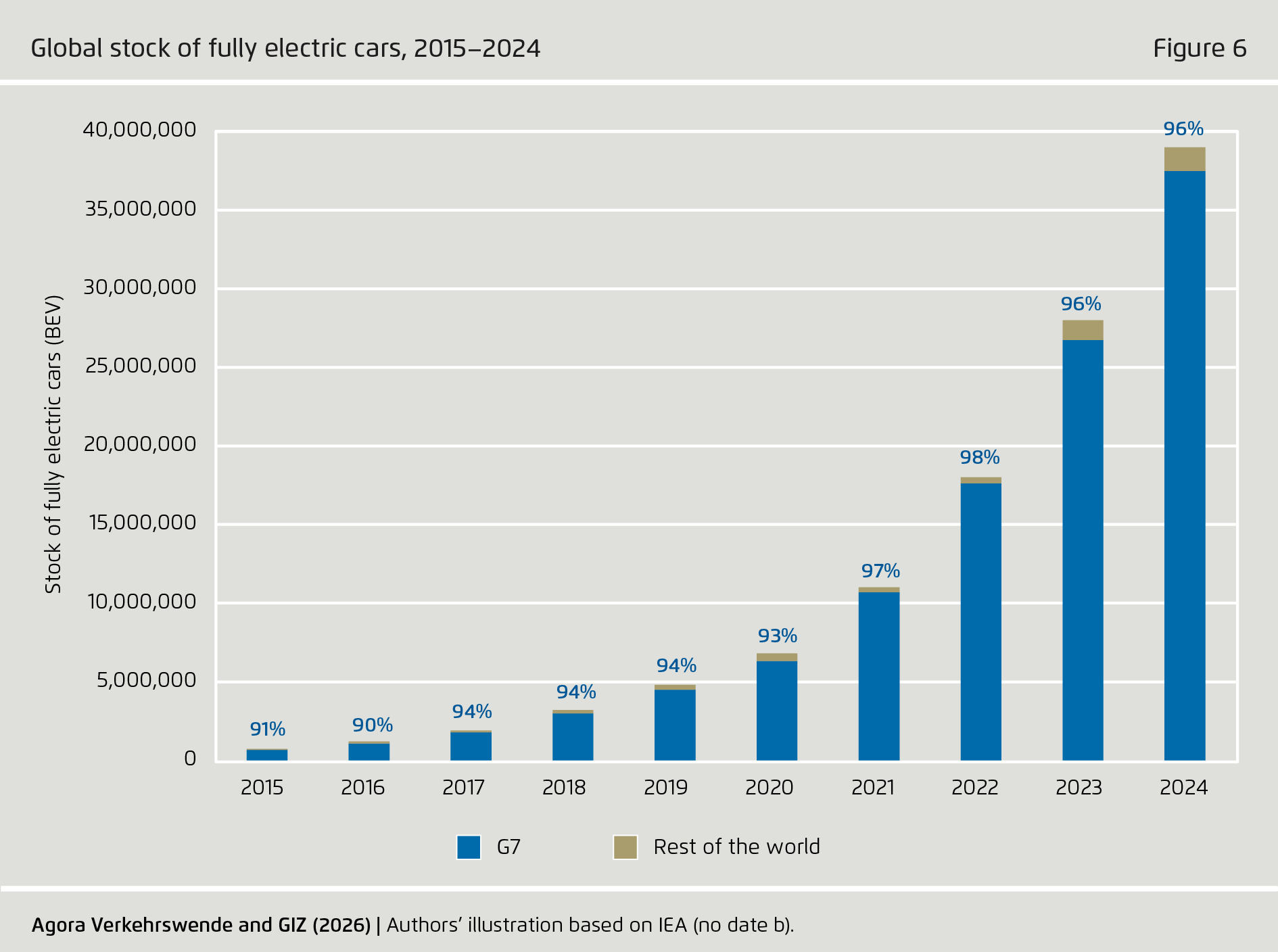

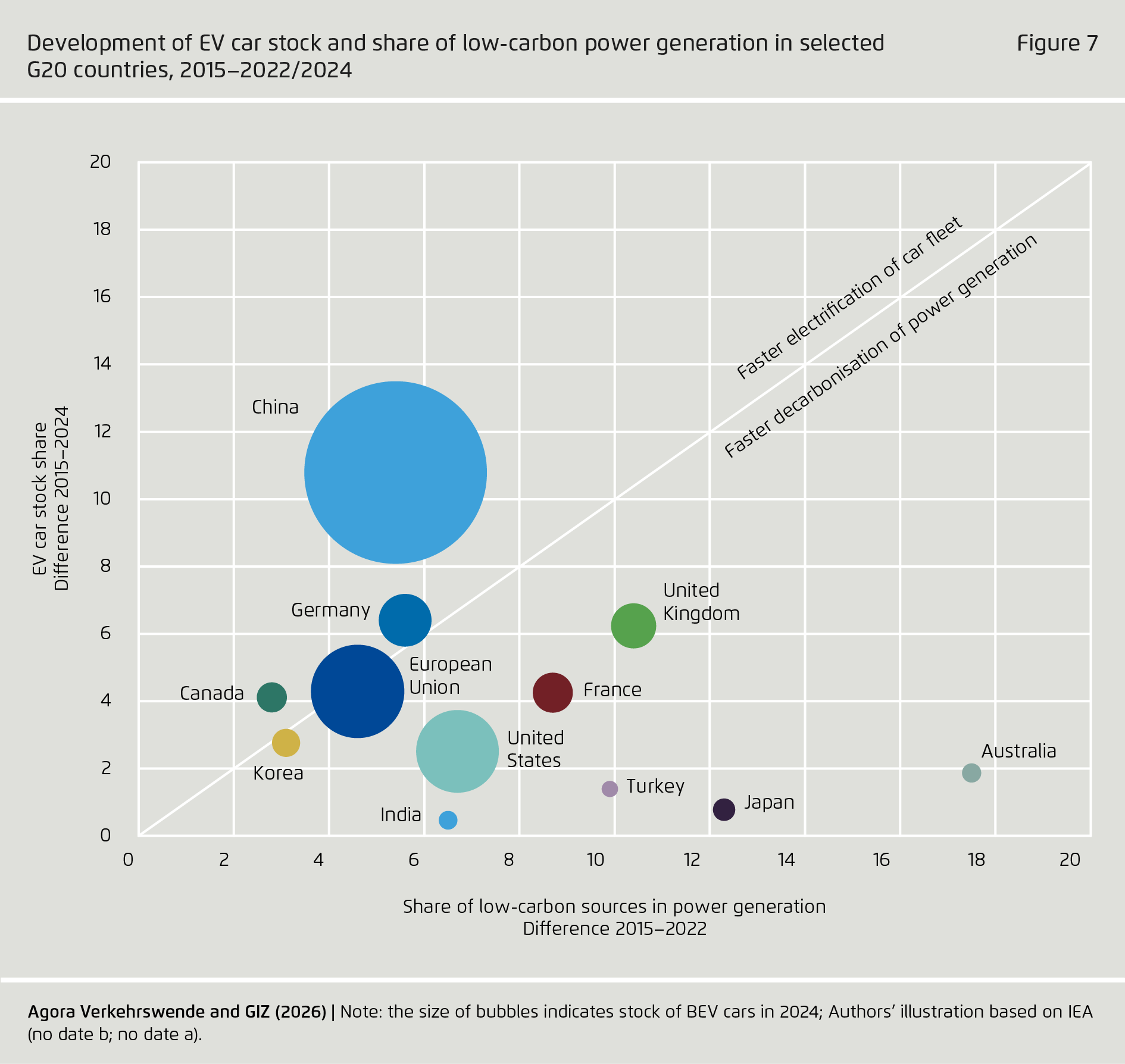

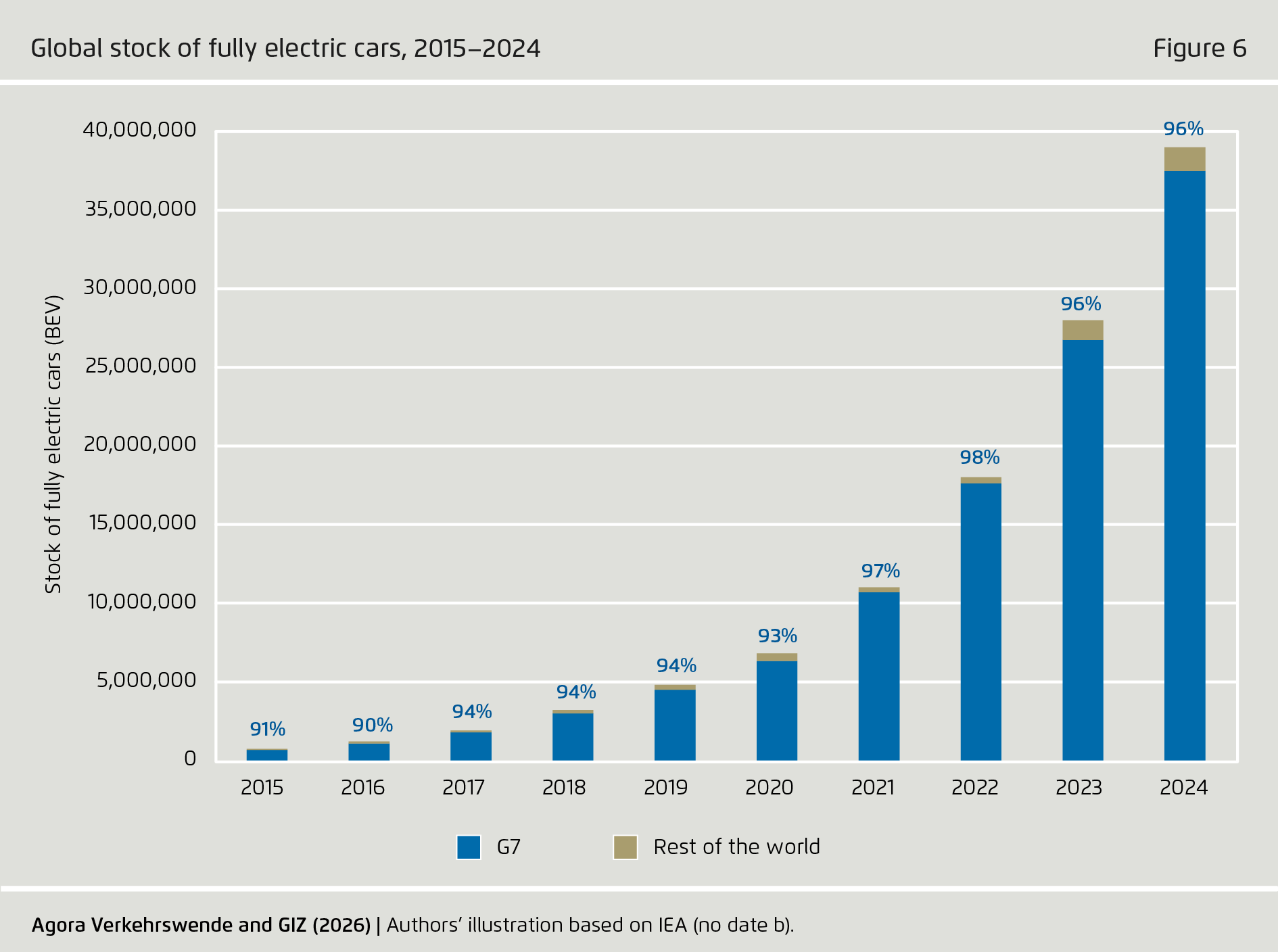

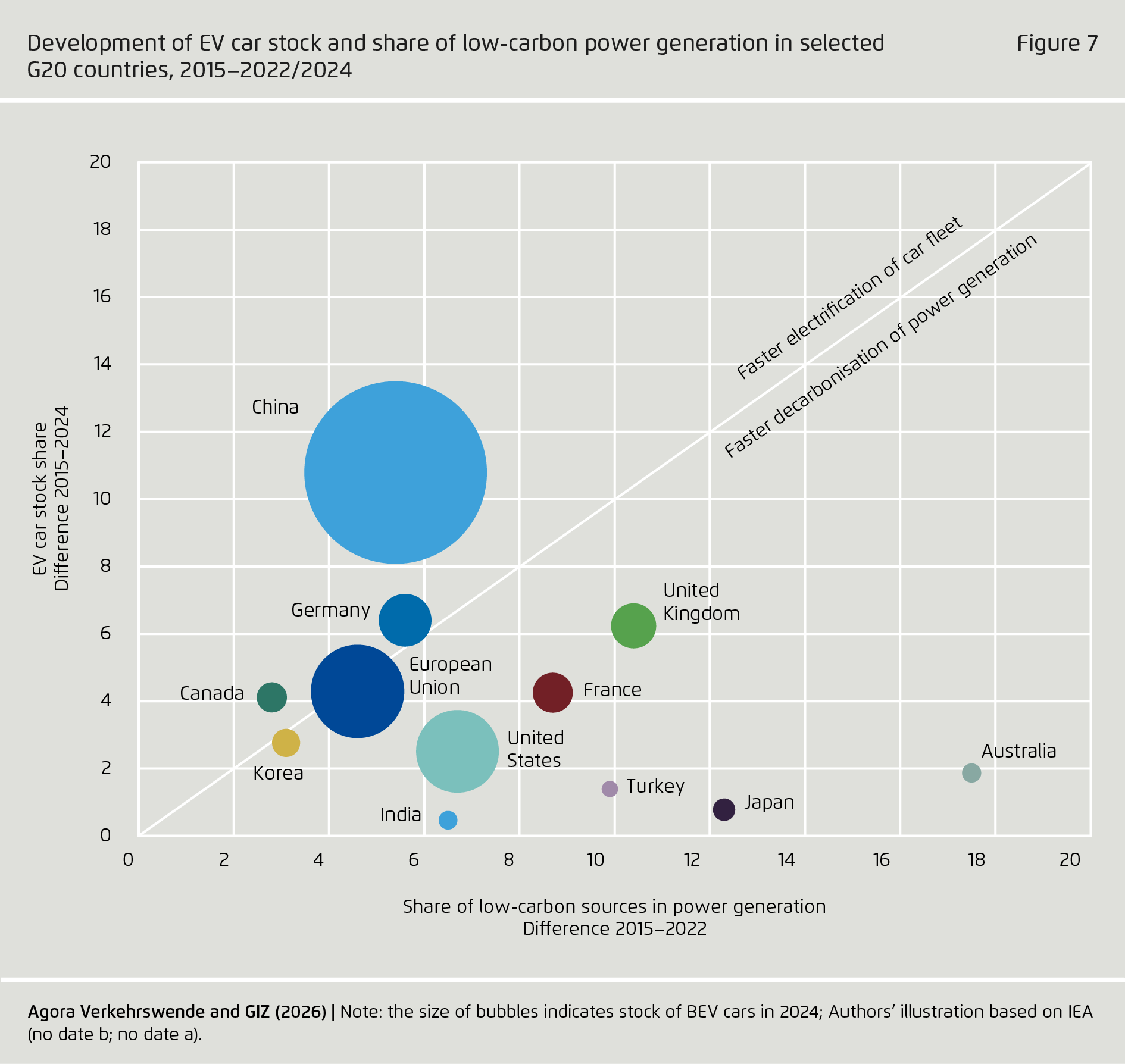

In 2015, electrification was still a niche technology globally. Only 730,000 fully electric cars, 100,000 buses, and 18,000 trucks were on the road. A decade later, the number of electric cars had grown to 39 million worldwide – an astonishing increase of over 5,000 %. Most of this growth occurred in G20 countries (see Figure 6). The largest growth market in the G20 is China: Between 2015 and 2024, China increased its share of electric cars in the total fleet from 0.2 % to 11 %. Germany, the United Kingdom, the European Union, France and Canada followed with increases of four to six percentage points over the same period. All other G20 countries progressed much more slowly in their efforts to electrify their car fleets (see Figure 7).

The electrification of vehicle fleets is a crucial element of transport-sector decarbonisation. Electric vehicles are more energy efficient than cars powered by fossil fuels; this efficiency means lower emissions. However, the full potential of electric vehicles can only be realised if they run on electricity generated with low-carbon technologies. Therefore, it is essential for the electrification of the transport sector and the decarbonisation of power generation to proceed in tandem.

Between 2015 and 2022,2 all G20 countries increased their share of low-carbon power generation, albeit at different rates. Italy was the exception, with coal and oil use in electricity generation3 increasing in 2022 due to the energy crisis affecting Europe. Australia, Japan4 and the United Kingdom achieved the highest growth in low-carbon power generation. Australia managed to more than double its share of low-carbon power generation from 13 % in 2015 to 31 % in 2022, but lags in electrification, where efforts to electrify the fleet started late compared to other countries. Over the same period, the United Kingdom increased its share of low-carbon power generation from 44 % to 54 %, while almost completely phasing out coal-fired power generation. Japan increased its share of low-carbon sources by mainly restarting previously closed nuclear power plants, but also by increasing its share of low-carbon power generation by 12 percentage points (see Figure 7).

1.4 Road transport continues growing

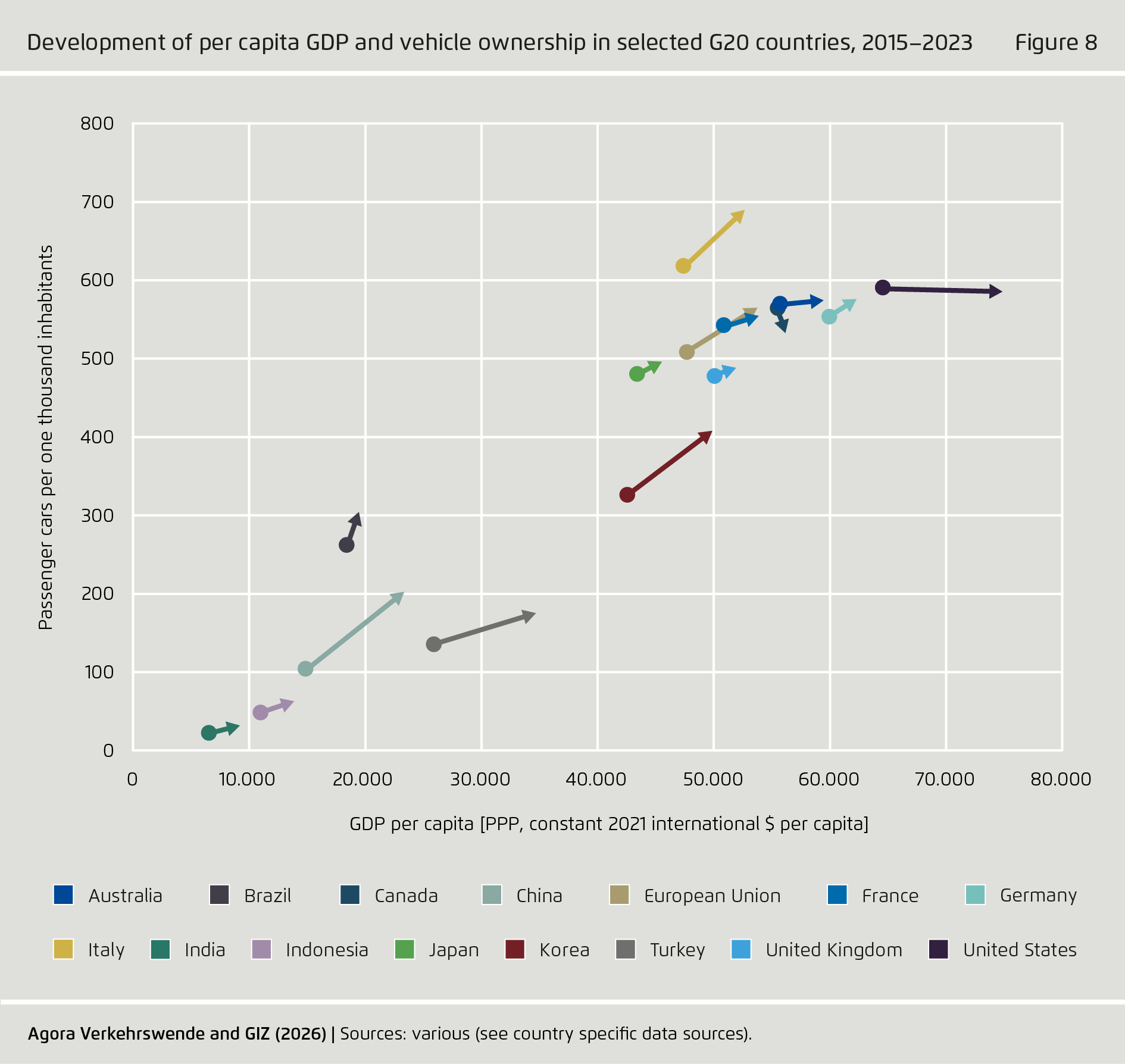

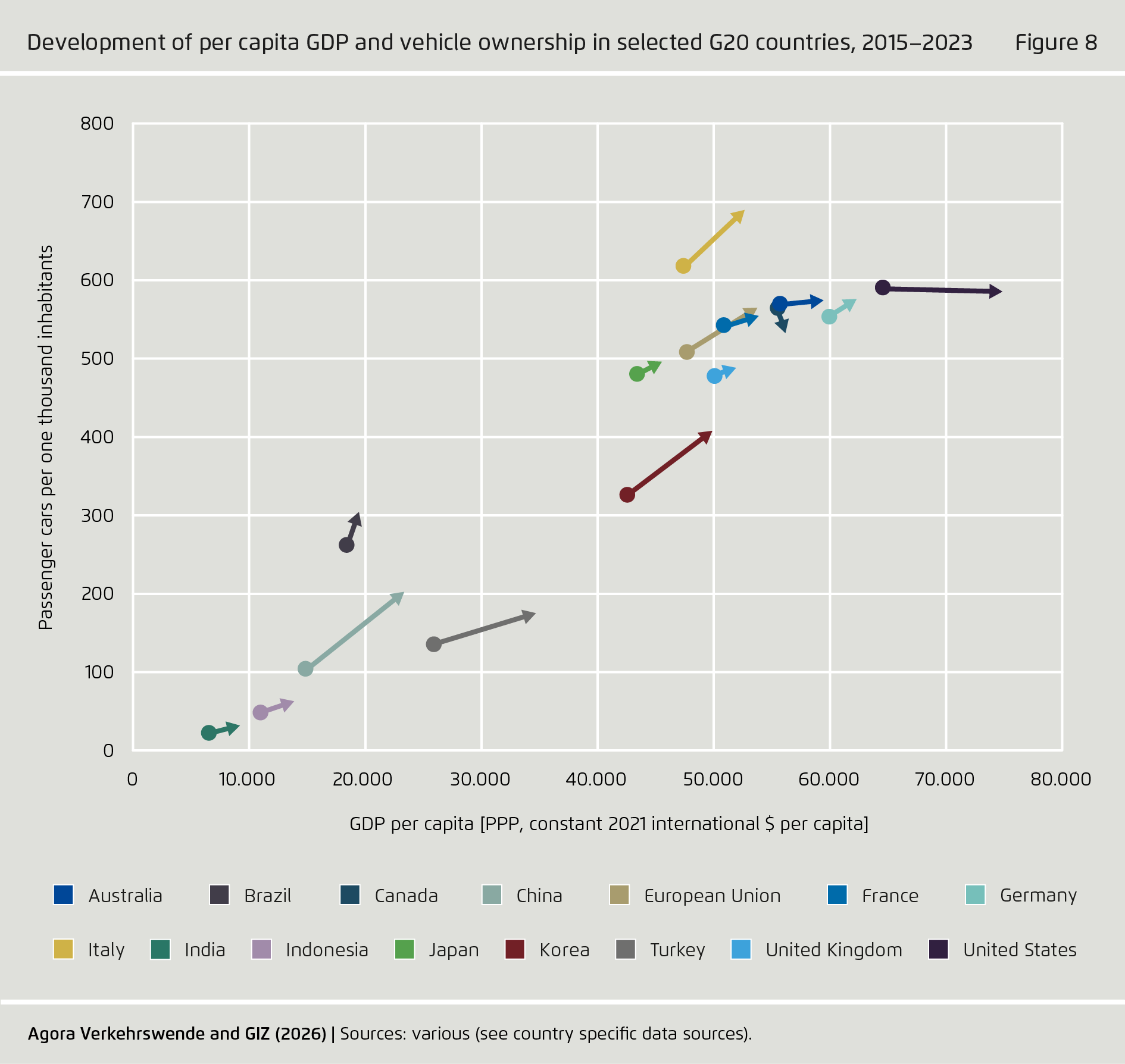

Replacing combustion-engine vehicles with electric ones is not enough to curb GHG emissions from the transport sector. We need to shift towards more efficient modes of transport, such as buses, rail and water-based transport, to use energy as efficiently as possible. The trend towards individual mobility is evident in all G20 countries, with the notable exceptions of Canada and the United States, where the number of passenger cars per 1,000 inhabitants decreased between 2015 and 2023 (albeit from high starting levels). Growth in motorisation is slowing in some of the analysed countries, particularly in those with a higher GDP per capita, such as Australia, France and the United Kingdom. However, even higher-income countries such as Italy and South Korea have experienced significant growth in the number of passenger cars, despite already high initial levels (see Figure 8).

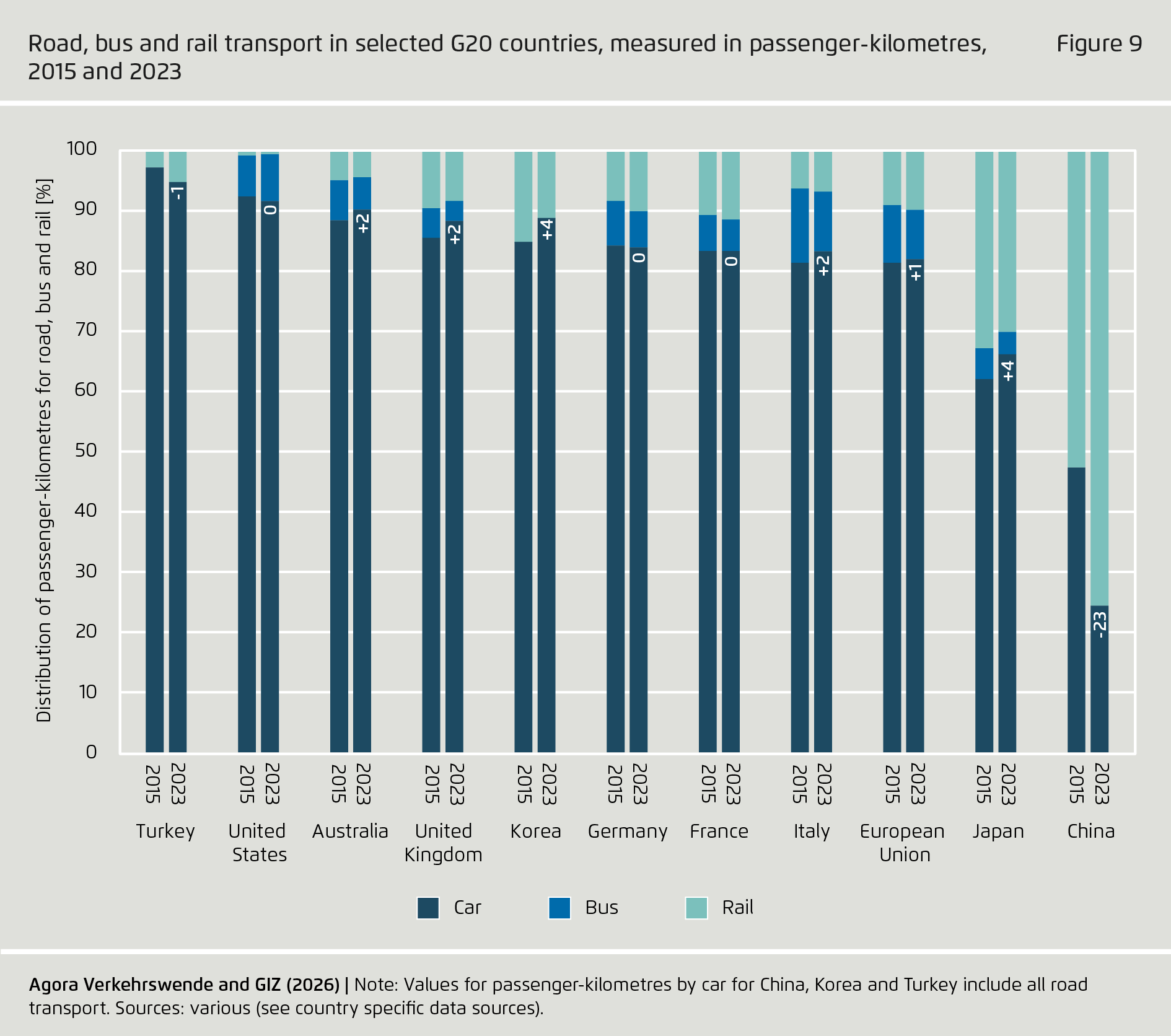

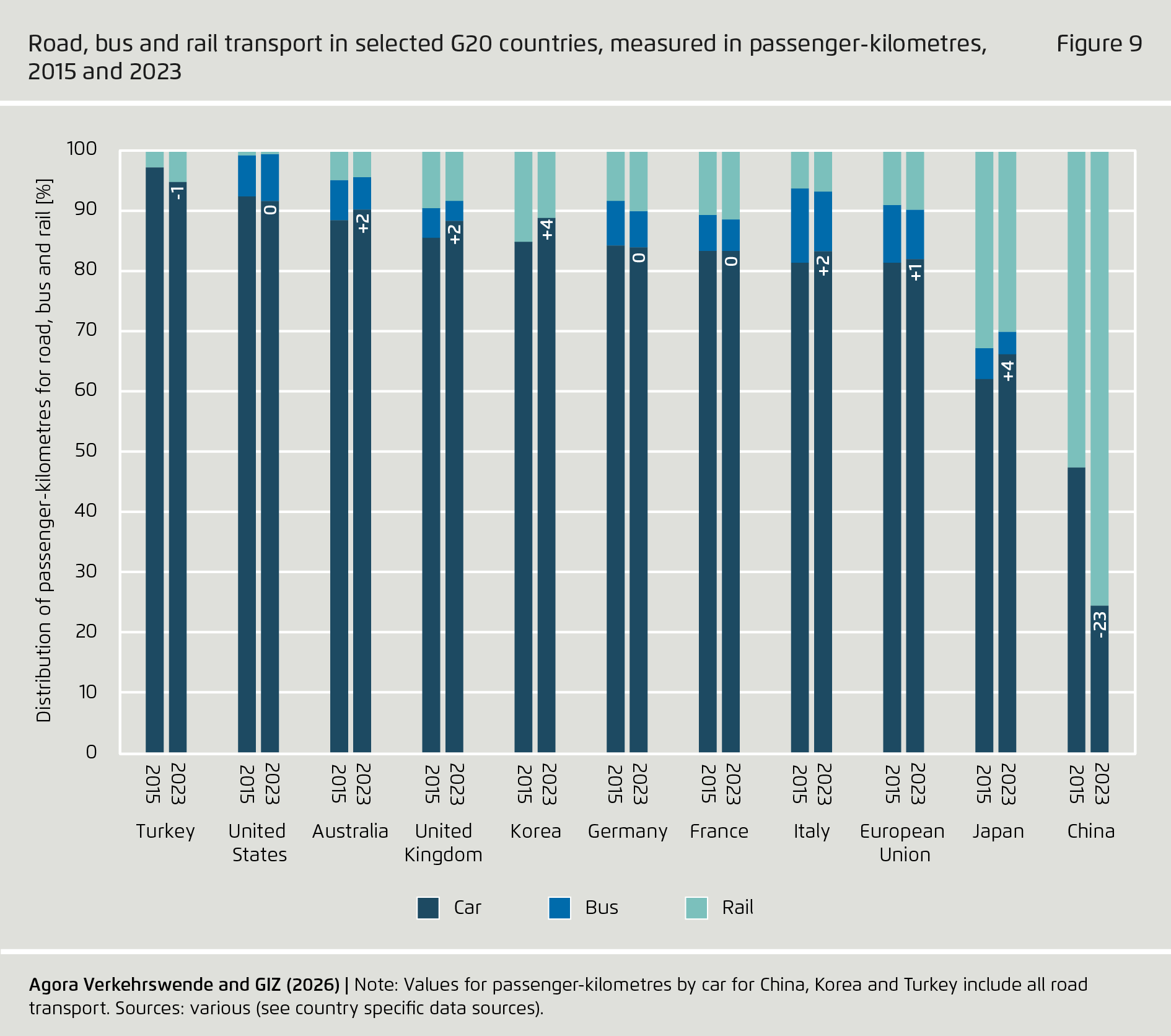

Nevertheless, vehicle ownership represents merely one aspect of the broader issue. The key factor in terms of emissions is how often and how far people drive their own vehicles, and how frequently they opt for alternative modes of transport, such as rail, which is the most energy-efficient form of passenger transport. Analysing the development of passenger transport activity levels for cars and railways since 2015 reveals mixed results.

Most G20 countries continue to rely heavily on cars for passenger transport, with shares above 80 %. Only Japan and China use rail to transport a significant proportion of passengers. Both countries have well-developed rail systems with substantial high-speed capacity. The importance of rail in China has increased significantly over the past decade. In 2015, rail already accounted for 53 % of land-based passenger transport, but rose even further, to 76 %, by 2023. Aside from China, Turkey is the only country to see a lower reliance on cars, but the shift in Turkey is small (one percentage point). All other G20 members maintained or increased their reliance on cars (see Figure 9).

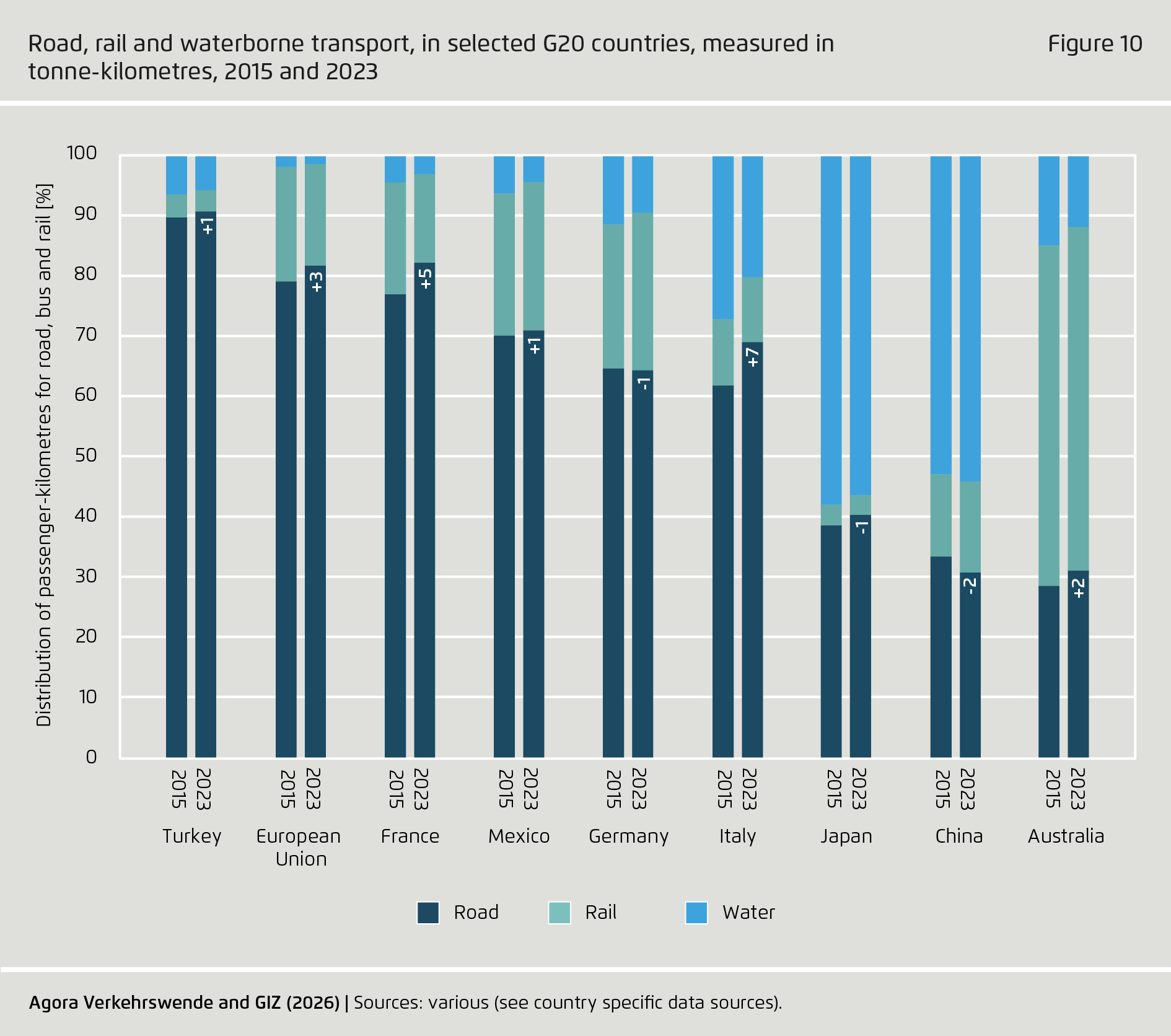

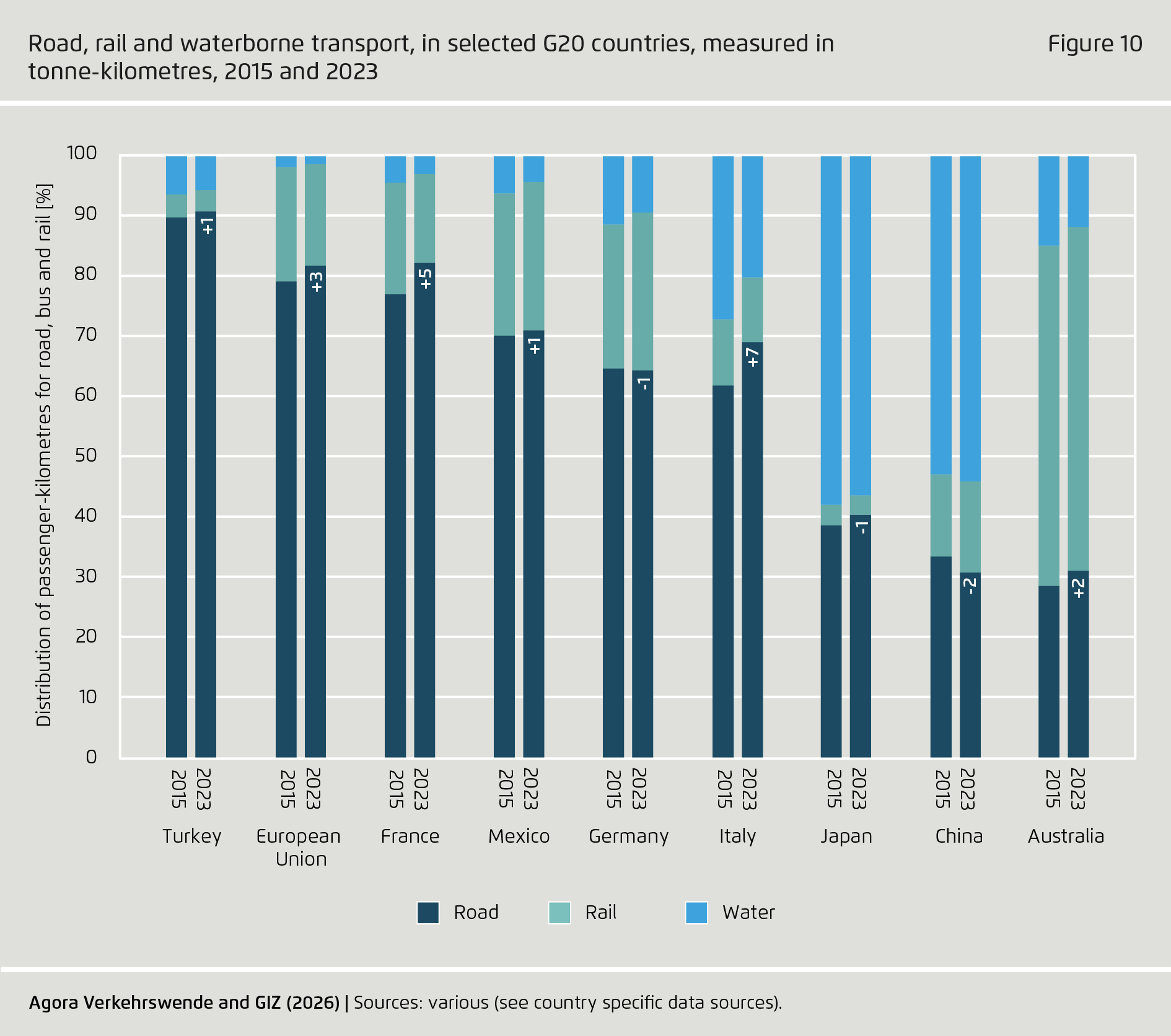

The majority of G20 countries place a similar emphasis on road transport for the purpose of moving goods. Over the past decade, the proportion of goods transported by road has increased in most G20 countries for which data are available, with the exception of China and Germany. In Germany, this is due to a 9 % overall decrease in tonne-kilometres over the period, as well as a 25 % drop in water-based transport. Conversely, China shifted a large proportion of its rapidly increasing freight volumes (which grew 39 % in 2015–2023) to rail and waterways, with coastal shipping accounting for a significant portion of this shift (see Figure 10).

Japan, China and Australia are the only countries that transport less than half of their goods by road. Australia mainly uses its rail system for this purpose, while Japan and China have strong waterborne freight systems. However, as of 2023, the much-needed shift towards more efficient modes of transport remains outstanding. Italy, France and the European Union as a whole are moving rapidly towards more road freight.

2 | Drivers for change

International commitments send important signals and can influence national policymaking. They are often translated into national targets, which are set out in strategies or binding legislation, as well as subsequent policy instruments. This report series has been tracking international and national commitments, as well as policies, since 2017. This edition will examine developments since the first report in more detail and assess how they are linked to the developments observed in section 1.

2.1 Quantitative transport sector targets are increasingly common

Nationally Determined Contributions (NDCs), which are voluntary commitments submitted by countries, are a key element of the Paris Agreement. The initial submissions in 2015 were mostly high-level and only included economy-wide targets. Since then, many subsequent NDC submissions have become increasingly detailed, providing GHG emission or other quantitative sector targets.

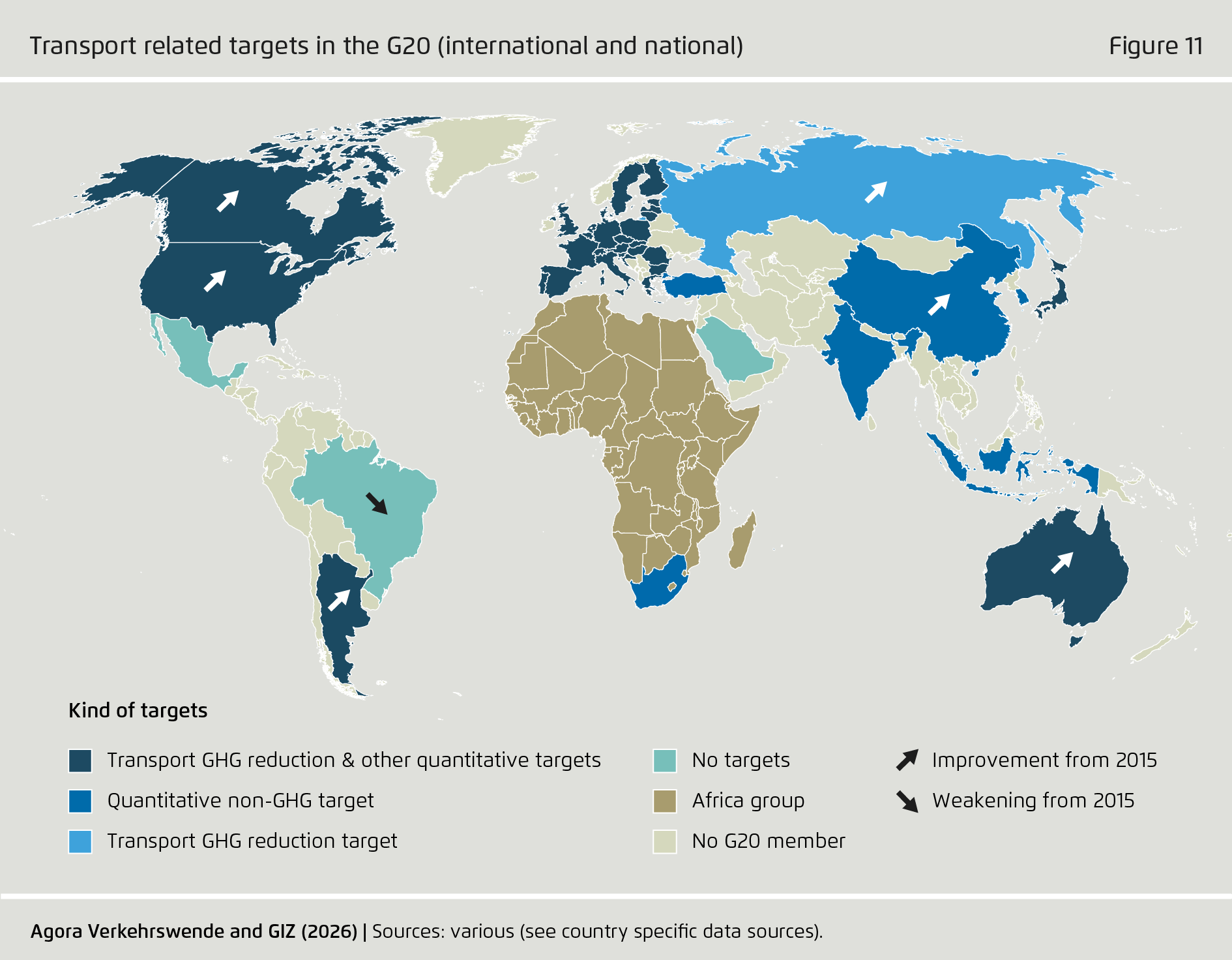

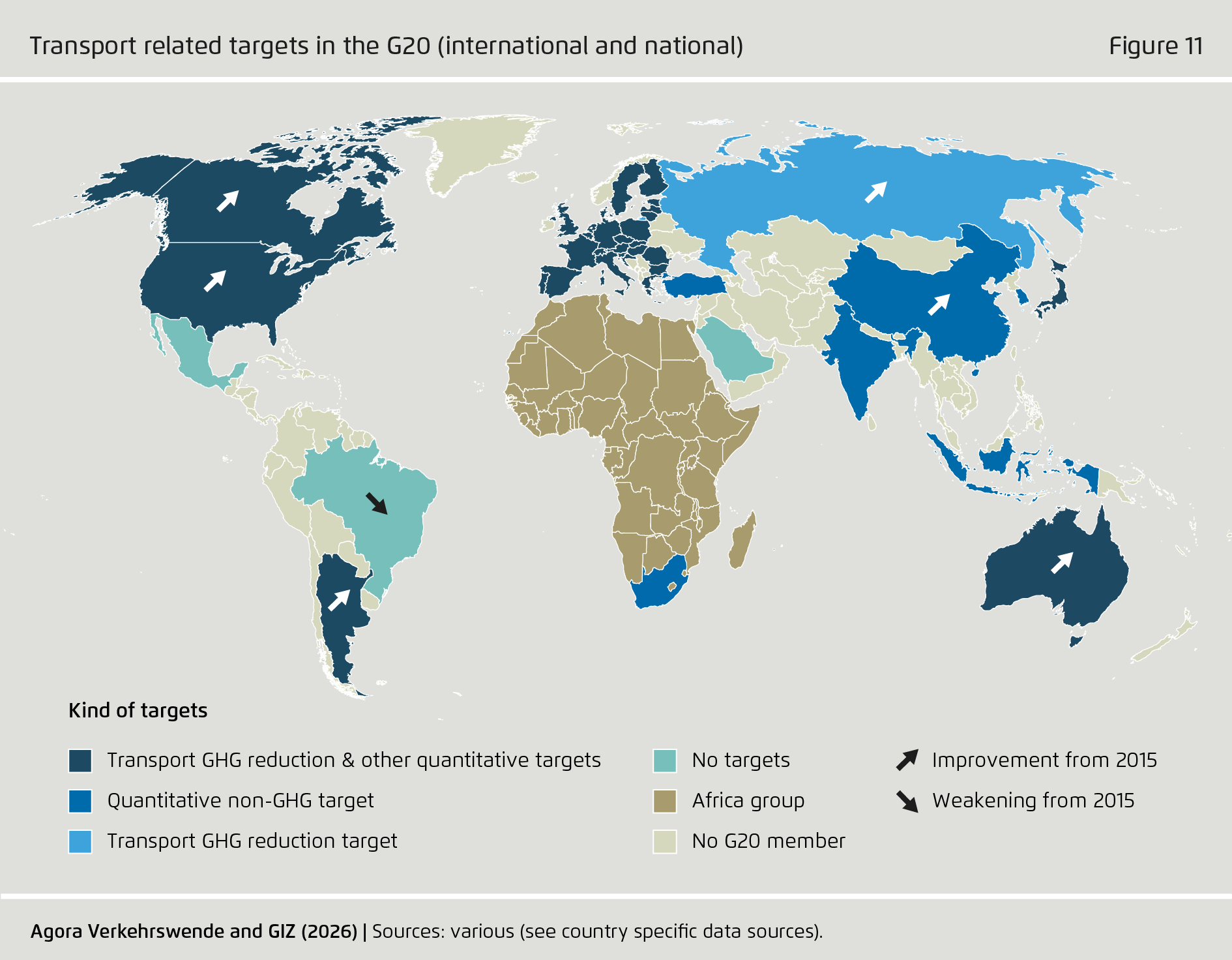

In the first round of NDCs, only five G20 countries (Brazil, China, India, Japan and South Africa) included transport-related commitments. Meanwhile, 12 G20 members already had some form of quantitative target at the national level at that time. By the end of 2025, a total of 17 of the G20 members had a quantitative target. In their latest NDC submissions, 13 countries included at least one quantitative target for the transport sector. Some of these targets are based on existing or have led to national legislation, such as the EU CO₂ emission standards for vehicles. A further four countries have quantitative targets at the national level only. Figure 11 provides an overview of targets set by G20 members either in NDCs or at the national level.

Overall, more countries are setting quantitative targets, particularly large economies such as China and the United States, across national and international targets. Brazil is the only country to have weakened its commitment in the transport sector. The 2008 National Climate Change Plan (PNMC) set a greenhouse gas (GHG) emission target for the transport sector for 2020. There are no comparable targets in place for later periods. Apart from Brazil, only Mexico and Saudi Arabia have no sector-specific targets in place, either nationally or internationally (see Figure 11).

A growing number of countries are setting GHG emission targets for the sector, but many also include non-GHG targets. In 2015, targets relating to vehicle efficiency, technology and renewable fuel were predominant. These remain important today, with a clear focus on increasing the proportion of zero-emission vehicles in the fleet (see the next section). However, targets to increase the proportion of sustainable modes of transport and expand rail infrastructure are becoming increasingly important in defining countries’ ambitions.

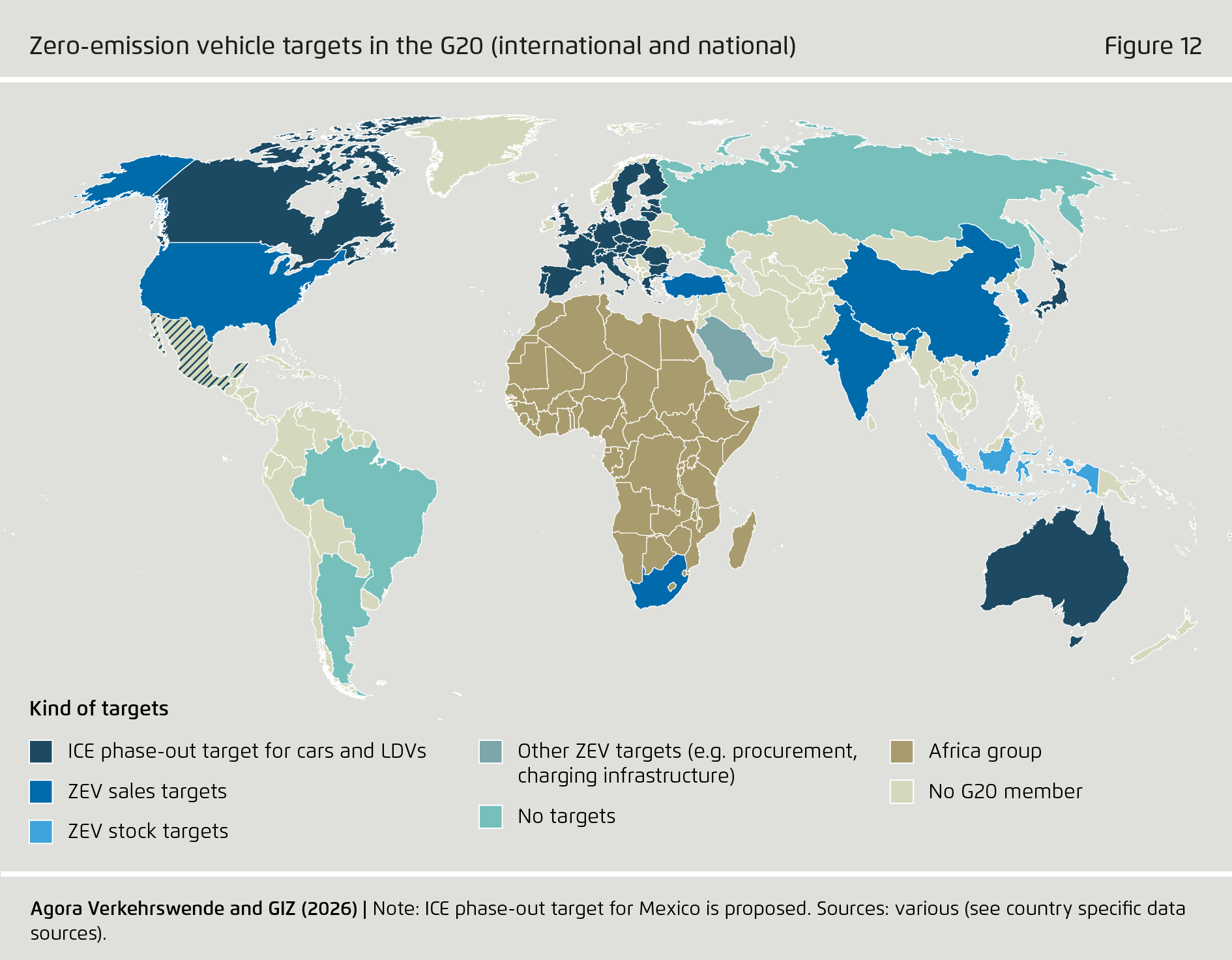

2.2 Zero-emission vehicle targets are widespread but eroding

The shift away from fossil-fuel-powered internal combustion engines (ICE) plays a key role in most countries’ decarbonisation strategies. Countries are adopting an open approach to technology, focusing on zero-emission vehicles that encompass all technologies leading to zero greenhouse gas (GHG) emissions at the tailpipe. This includes hydrogen-powered vehicles, either directly or via fuel cells. Depending on the country, it can also include plug-in hybrids (PHEVs) or electric vehicles with range extenders.

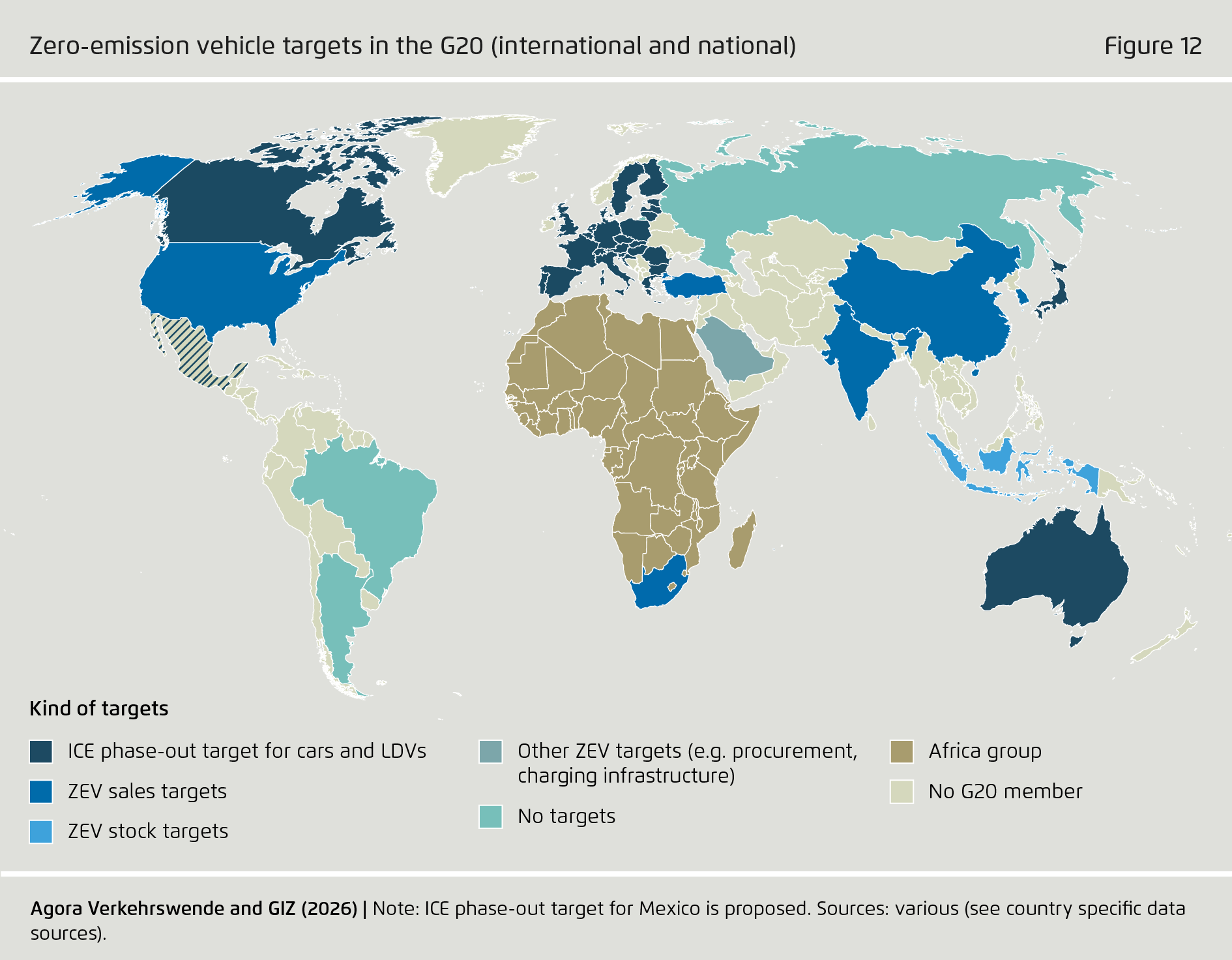

A closer look reveals that the approaches to setting zero-emission vehicle targets vary greatly. Only four countries – Argentina, Brazil, Russia and South Africa – have not yet set any targets relating to electrification or zero-emission vehicles. At the other end of the spectrum, Australia, Canada, the European Union, Japan and the United Kingdom are aiming to achieve a sales share of 100 % for zero-emission passenger cars and light-duty vehicles (LDVs) by 2035. However, the European Union is currently in the process of revising its regulation, and will likely reduce the requirement to 90 % by 2035. Mexico proposed legislation in 2022 that would see 50 % of passenger vehicle sales to be electric by 2030 (including hybrids and PHEVs), 100 % to be PHEVs and BEVs by 2040, and 100 % of vehicles sold being fully electric by 2050, but this legislation has not yet been adopted.

Although China, India, South Korea, Turkey and the United States have set targets for zero-emission vehicle (ZEV) sales, they have not determined a date by which internal combustion engine (ICE) vehicles will no longer be sold. China plans to achieve a “new energy vehicles” sales share of 80 % by 2030. India is focusing on vehicle segments other than cars and has various EV sales targets for 2030 (30 % of passenger vehicles, 70 % of commercial vehicles, 40 % of buses, and 80 % of two- and three-wheelers). South Korea aims to achieve an 83 % market share for new passenger vehicles by 2030, while Turkey is aiming for 35 %. By contrast, support measures to achieve higher EV sales have been revoked under the current administration in the United States. Indonesia has set targets for its vehicle fleet, aiming to have 2.2 million electric cars and 13 million electric motorcycles on the road by 2030. Saudi Arabia’s Public Investment Fund (PIF) plans to manufacture 500,000 electric vehicles (EVs) annually by 2030. Many countries have additional public procurement targets.

To be sure, the reversal of policy in the United States and contemplated weakening of CO₂ emission standards in the European Union are a setback for continued global progress. However, faltering ambition in the United States and European Union will be more than offset by the many emerging, developing and advanced economies that are now embracing electrification. This will lead to corresponding changes in the global automotive market, as value creation shifts to countries best able to satisfy surging demand for electric vehicles.

2.3 Increasing action is yielding visible results – but only in certain areas

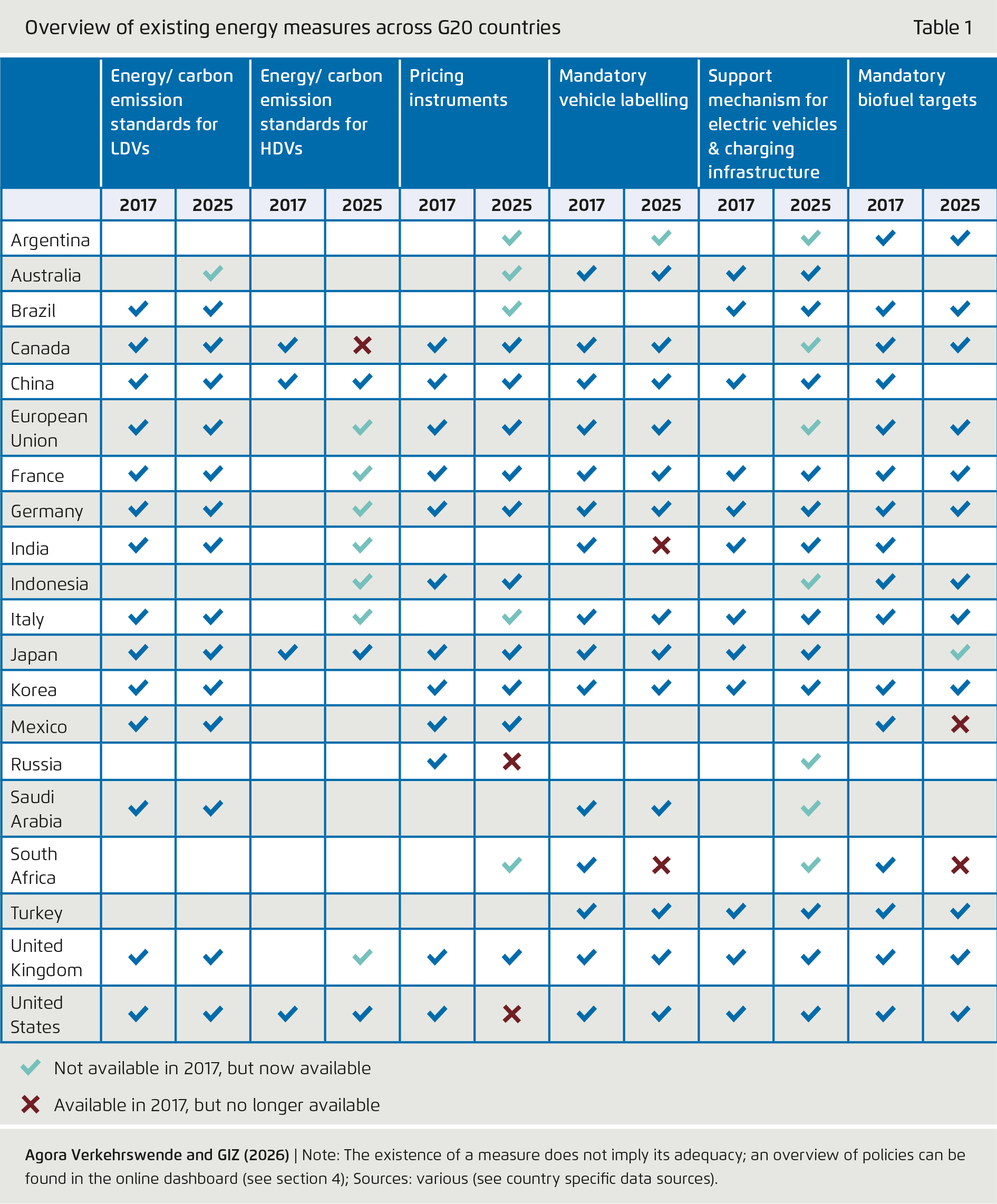

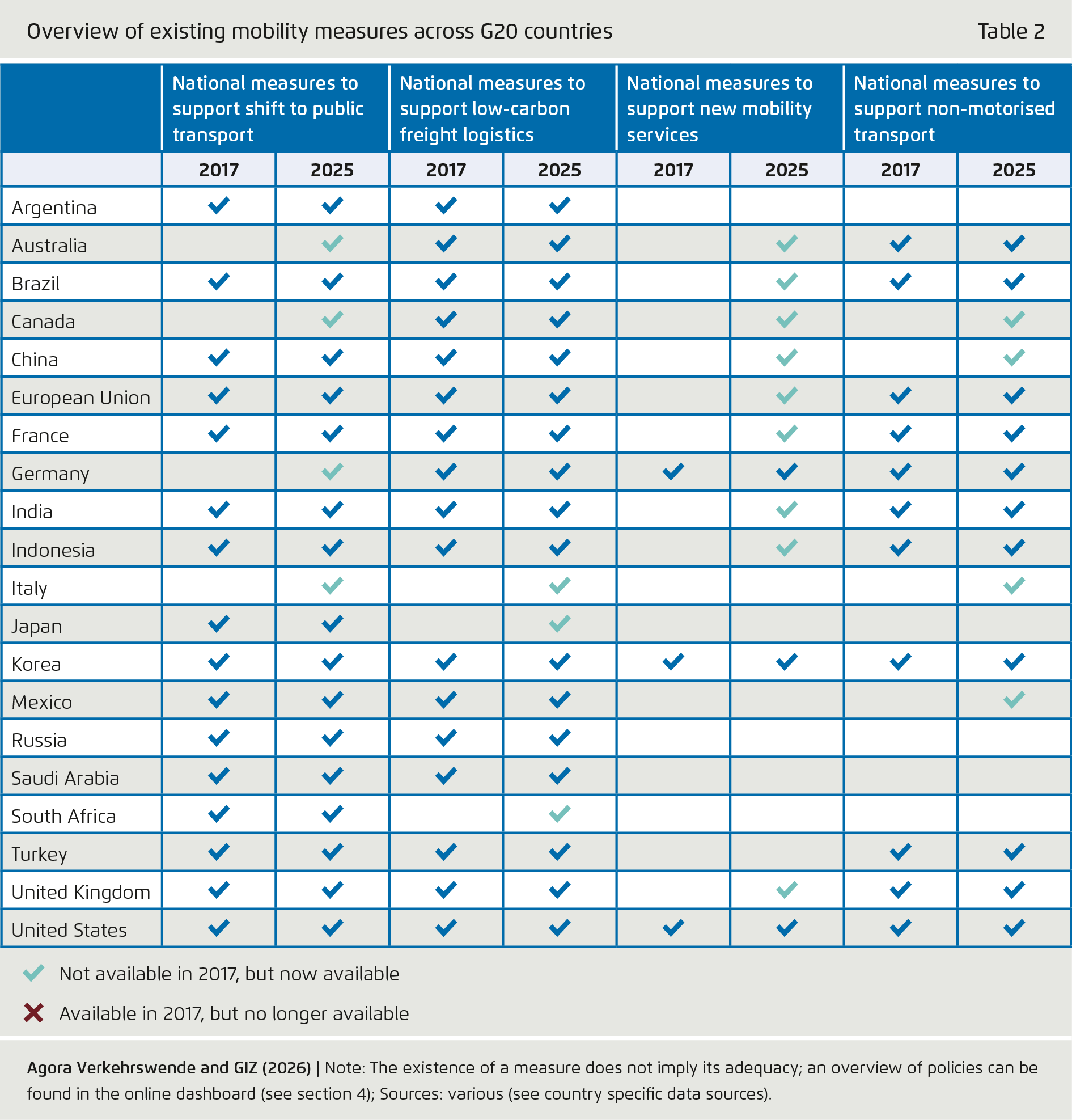

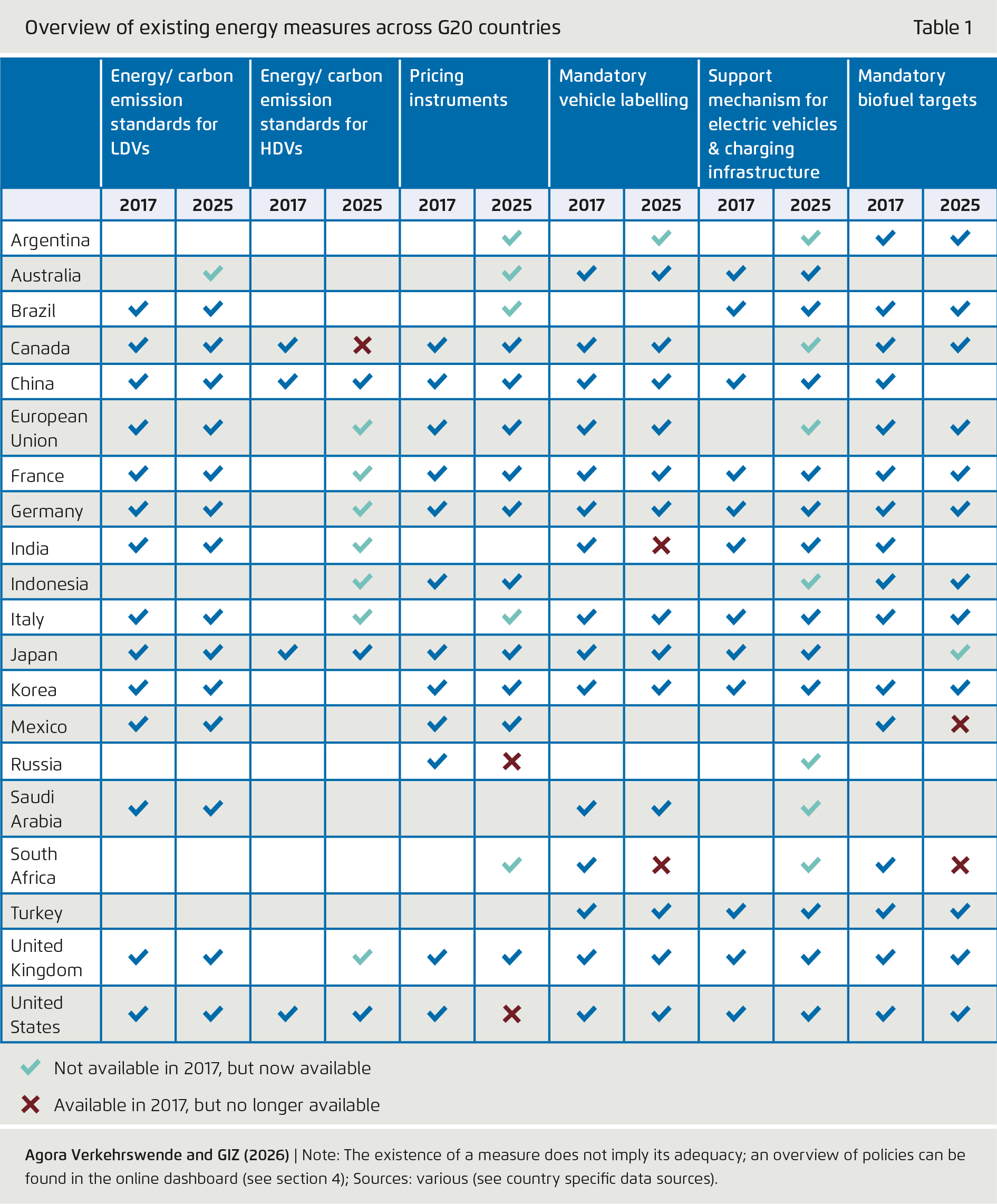

Targets are just the first step for driving change. The national implementation of actual policy instruments is essential for tangible emission reductions to be achieved. Compared to the first stocktake published in 2017, a larger number of countries are now implementing policies that aim to reduce greenhouse gas (GHG) emissions in the transport sector.

All G20 countries aside from Mexico have policies to support EVs. This is reflected in the increasing number of new EV registrations and growing size of EV fleets over the past decade (see section 1.3), although most countries started from a very low baseline in 2015. Most countries provide financial incentives for vehicle buyers. These incentives can take the form of reduced import duties, lower ownership or vehicle taxes, reduced purchase taxes, or direct rebates. Some governments also prioritise electric vehicles for public fleet procurement. Countries are also increasingly supporting the domestic manufacturing of EVs.

Energy and CO₂ emission standards for light and heavy goods vehicles (LDVs and HDVs) have not yet been universally adopted, despite their importance for the transition to more efficient, low-carbon vehicles. However, there is also good news. Australia enacted the New Vehicle Efficiency Standard Act in 2024 for passenger cars and light-duty vehicles. Since the first stocktake, seven countries (the European Union and its member states, India, Indonesia and the United Kingdom) have implemented energy or carbon emission standards for heavy-duty vehicles (see Table 1).

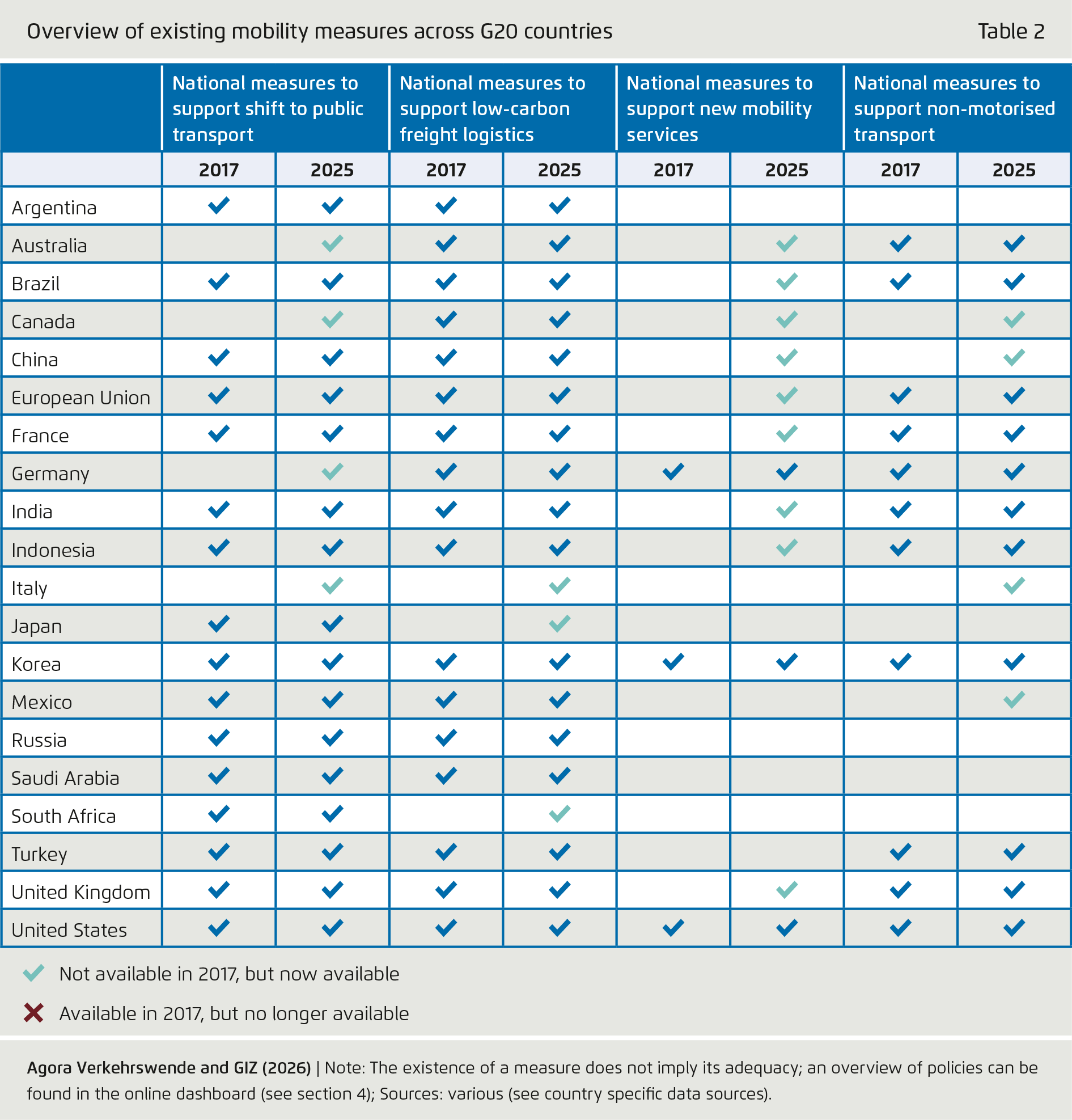

Although policies to support modal shift are gaining traction, they are not yet delivering what is needed. All G20 countries now have policies that support a shift to public transport and low-carbon freight logistics, including those that did not have such policies in place in 2015. Some of these policies have only recently been introduced, such as Australia’s National Urban Policy, adopted in 2024, and the Canada Public Transit Fund (CPTF). Indonesia has also recently planned to expand its short-sea shipping network in order to reduce price disparities and shift freight to maritime transport. Due to the lengthy implementation times of public transport infrastructure projects, it will take many years for these policies to have an observable effect. Nevertheless, it is crucial that all countries now have support and expansion plans in place for public transport and low-carbon freight (see Table 1).

An increasing number of countries are also establishing legal frameworks and support systems for new mobility services, such as shared mobility. These mostly consist of legislation enabling and regulating such services. Measures to support active transport often focus on overarching strategies. Nevertheless, some countries have dedicated budget lines for expanding bike lanes and pedestrian infrastructure. Examples include Australia’s Active Transport Fund, Canada’s Active Transportation Fund, and the United Kingdom’s Cycling and Walking Investment Strategy.

As outlined in section 1.4, however, individual road transport remains prevalent for passengers and freight in most G20 countries. This suggests that the existing measures may have slowed down, but have not yet reversed, the trend, and that further efforts are required to provide appealing alternatives to driving or transporting goods by truck.

3 | Spotlight on Africa

Over the next five years, Africa’s economic growth is set to outpace the global average, and will only be surpassed by Asia. In 2023, Africa’s growth was more than eight times that of Europe and about three times that of North America. Six of the world’s ten fastest-growing economies are located on the continent. The African Continental Free Trade Area (AfCFTA), launched in 2021, is set to create a vast, single, integrated market.

Against this backdrop, in September 2023 the African Union transitioned from its guest status to become a permanent G20 member. Over the past two years, the AU has prioritised reforming global financial institutions, ensuring food security, facilitating a fair energy transition and promoting trade and investment through the AfCFTA. The AU has also worked to improve sovereign credit ratings and expand investment in vaccine manufacturing, pharmaceuticals and pandemic preparedness.

For the first time, G20 leaders met on African soil under South Africa’s presidency, adopting a declaration that reaffirmed commitments to multilateral cooperation. Despite difficult geopolitical conditions, the summit, held under the slogan “Solidarity, Equality and Sustainability”, focused on priorities central to developing countries, particularly in Africa. These included debt reform, climate resilience, inclusive development, democratic global governance, climate action, food security, artificial intelligence and equitable critical mineral supply chains.

3.1 The role of Africa in climate action on transport

Africa is a growing giant, with a population predicted to reach at least four billion by 2100, up from around 1.5 billion in 2024.5 It has the youngest population, with an estimated median age of 19 across countries. This population growth, coupled with rising incomes and an expanding middle class, will significantly boost demand for mobility and transport.

Africa’s total emissions doubled between 1990 and 2024.6 A major driver of this trend is the transport sector, which accounted for 346 million tonnes of CO₂ emissions in 2024 – roughly one-third of the continent’s energy-related emissions. With transport-related emissions – the majority of which are attributable to motor vehicles – expanding nearly twice as fast as power plant emissions,7 transport’s growing carbon footprint threatens to derail climate policy goals.

Motorisation rates in Africa nevertheless remain low. On average, there are 73 vehicles for every 1,000 people in Africa, but this figure is expected to double by 2050.8 Only three countries are considered to be motorised: South Africa, Botswana and Libya. Meanwhile, Namibia, Morocco and Egypt are among those motorising rapidly, and Nigeria, Kenya and Zambia are predicted to become motorised in the future.9

3.2 Improving public transport and access to mobility remains the focus

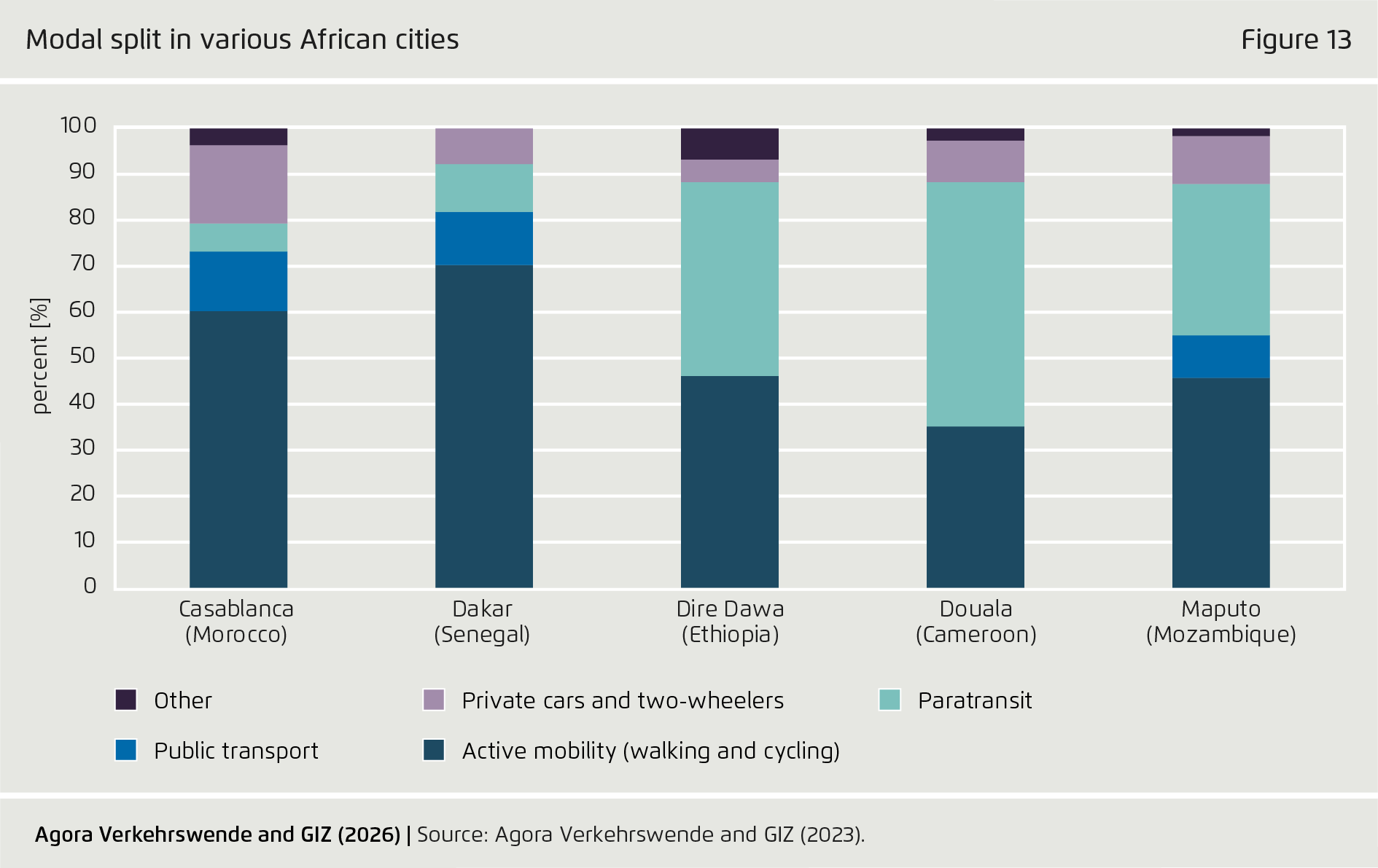

In many African cities, access to reliable, safe and affordable public transport remains a challenge. While many cities have scheduled bus services, paratransit often dominates public transport. For example, paratransit carried over 80 % of commuters in Kampala in 2015 and accounted for 58 % of trips in Cape Town, 86 % in Accra and 87 % in Nairobi.10 The major challenges associated with informal transport include poor safety, a high risk of accidents, low levels of comfort and limited accessibility. These issues are exacerbated by ageing vehicle fleets, inadequate infrastructure, manual payment systems, poor route planning and limited regulation.

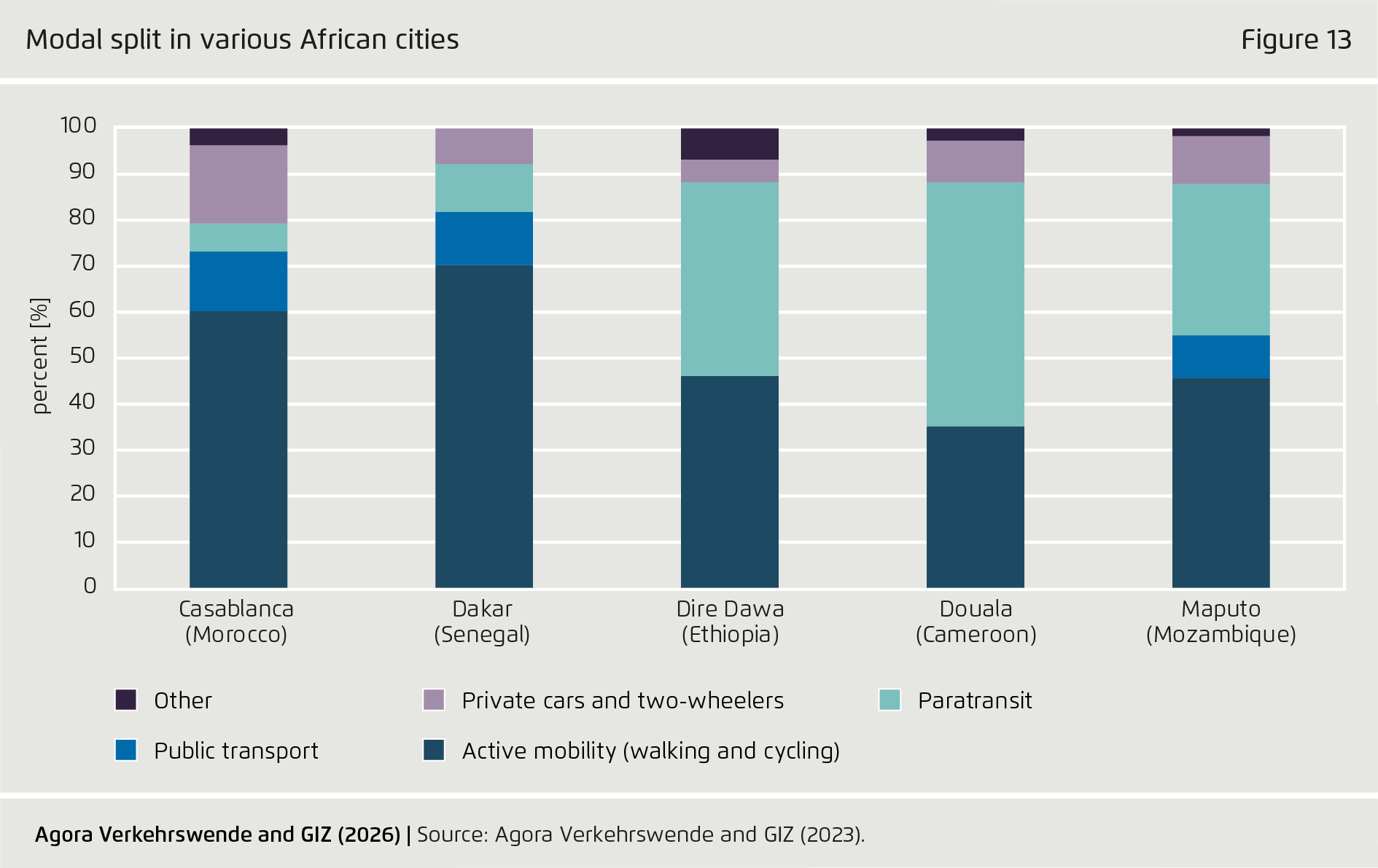

To address these issues, countries have introduced policies to enhance the accessibility and affordability of public transport. They are also working to reform and regulate paratransit while integrating land-use and transport planning. Figure 13 shows the modal split in selected African cities, with Dakar in Senegal having the highest share of active mobility at 70 %. However, this often directly relates to a lack of access to mobility and opportunities, as people are limited in the radius of activities they can undertake. The largest share of paratransit is in Douala, Cameroon, at almost 90 %. Here, as well as in Dire Dawa, Ethiopia, there is no public transport. Private vehicle ownership remains very limited across all cities.

Several large African cities have successfully upgraded their public transport systems, particularly by implementing Bus Rapid Transit (BRT) schemes. This reflects the dominance of road-based transport, as well as some investment in active mobility and light rail. BRT systems are operational or planned in many African countries, including Nigeria, South Africa and Tanzania. Lagos introduced one of Africa’s first BRT corridors in 2008: a 22 km system combining segregated, marked and mixed-traffic lanes to ease congestion. Dar es Salaam operates one of the region’s most successful silver-rated full BRT systems. Phase 1 carries around 200,000 passengers daily, and Phase 2 is under construction. South Africa boasts the most extensive BRT network, comprising Rea Vaya in Johannesburg, MyCiTi in Cape Town, and A Re Yeng in Tshwane, which together serve tens of thousands of passengers daily.11

Cities are also beginning to electrify public transport while continuing to invest in system and infrastructure improvements. Dakar in Senegal has launched Africa’s first fully solar-powered BRT system, which is expected to carry around 300,000 passengers per day, reduce average journey times from 95 to 45 minutes and operate 144 electric buses.12 In Kenya and Rwanda, BasiGo has deployed 25 electric buses which have logged over 1.6 million kilometres, carried more than 2.5 million passengers and avoided over 800 tonnes of CO₂ emissions while improving service quality.13 In South Africa, Golden Arrow Bus Services has ordered 120 electric commuter buses for Cape Town, and the City of Cape Town has awarded a contract to supply 30 low-floor electric buses for the MyCiTi system.14

3.3 Electrification is a major opportunity for African economies

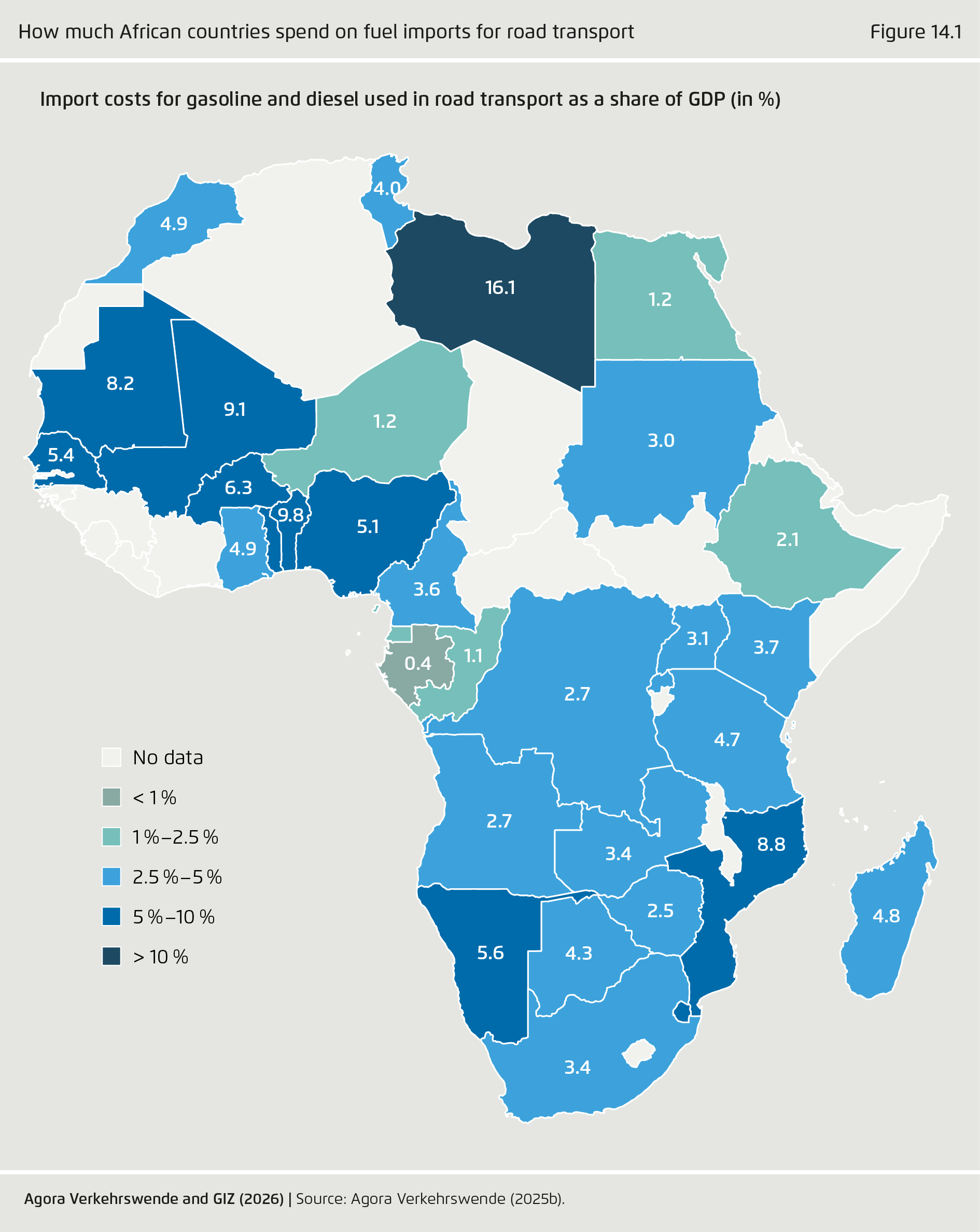

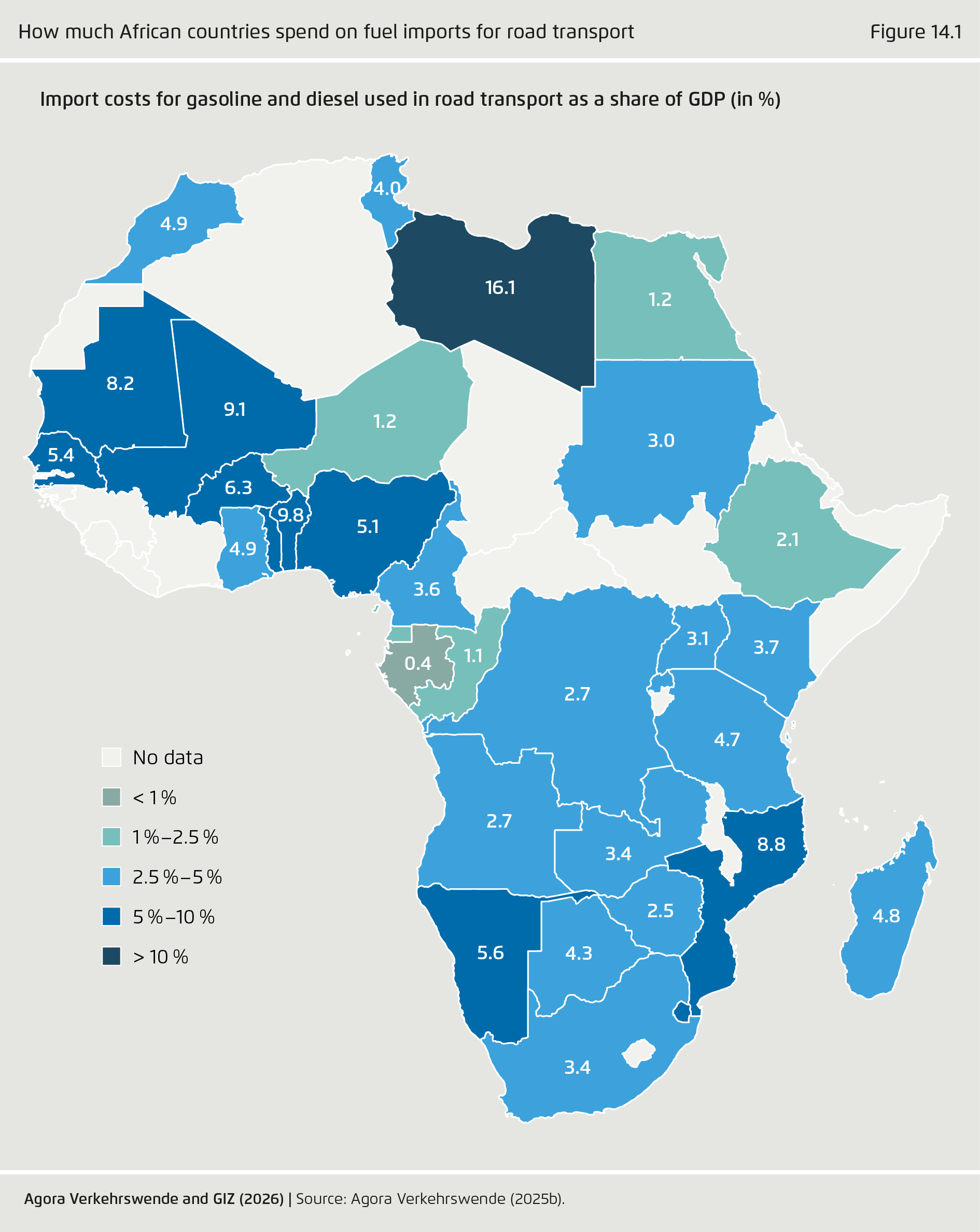

Africa is the world’s largest market for used vehicles, importing around 900,000 used passenger cars each year. These cars make up 85–90 % of light-duty fleets in most African countries.15 Between 2015 and 2018, around 40 % of the 14 million used light-duty vehicles exported globally were received by Africa, mainly from the EU, Japan and the United States.16 At the same time, African countries spend a disproportionately high share of their GDP on imported road fuels – 3.6 %, on average, compared to a global median of 2.1 % – yet transport access remains limited. High fuel import costs push up transport prices and often lead to subsidies that put a strain on public budgets and reduce resources for sustainable transport and development.17

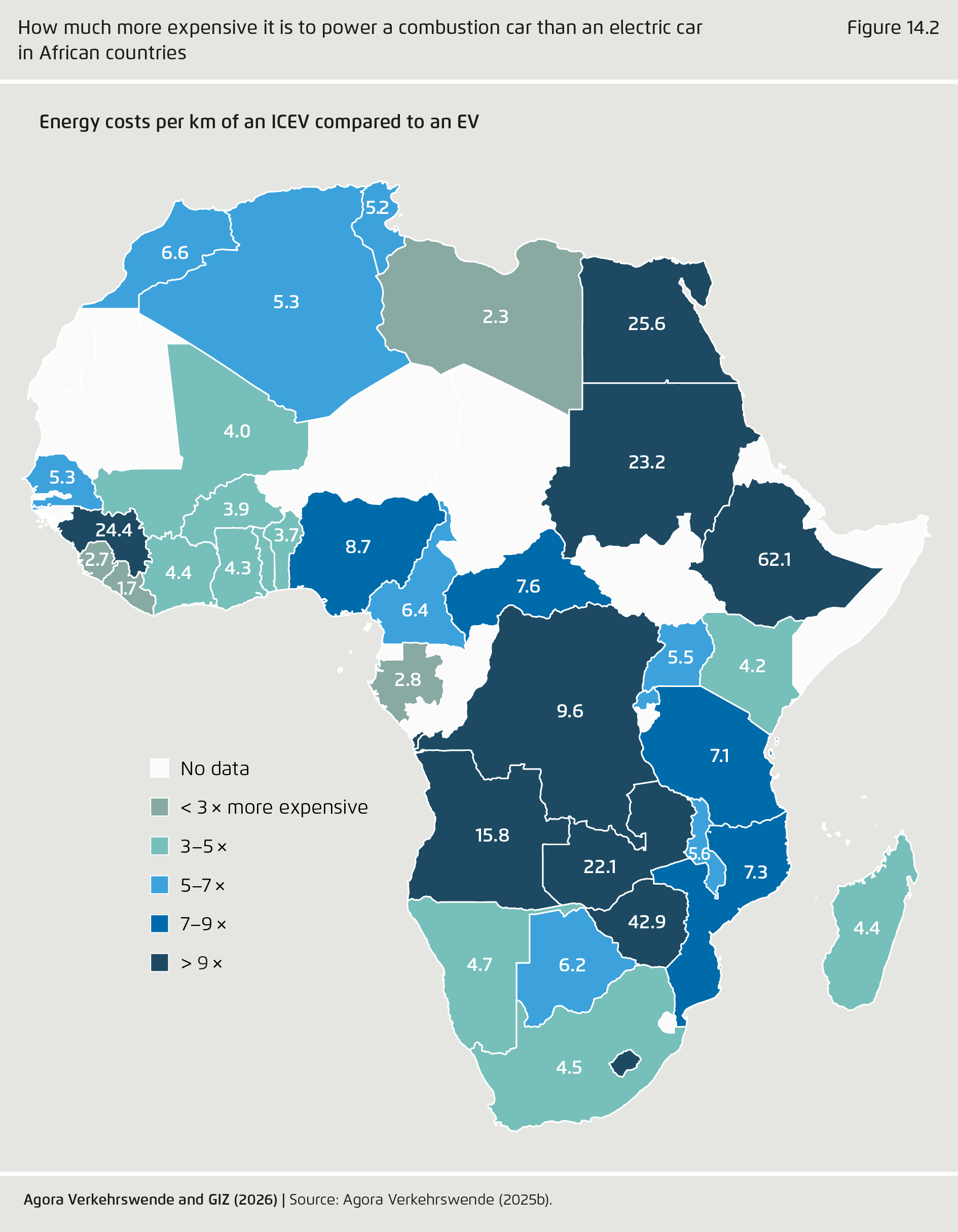

Figure 14.1 illustrates the proportion of GDP spent on importing gasoline and diesel for road transport in countries across Africa. Libya spends the highest proportion, at 16.1 % of GDP, followed by Mali (9.1 %) and Mozambique (8.8 %). As fuel imports are paid for in foreign currency and are subject to volatile global prices, they put significant pressure on national fiscal resources.

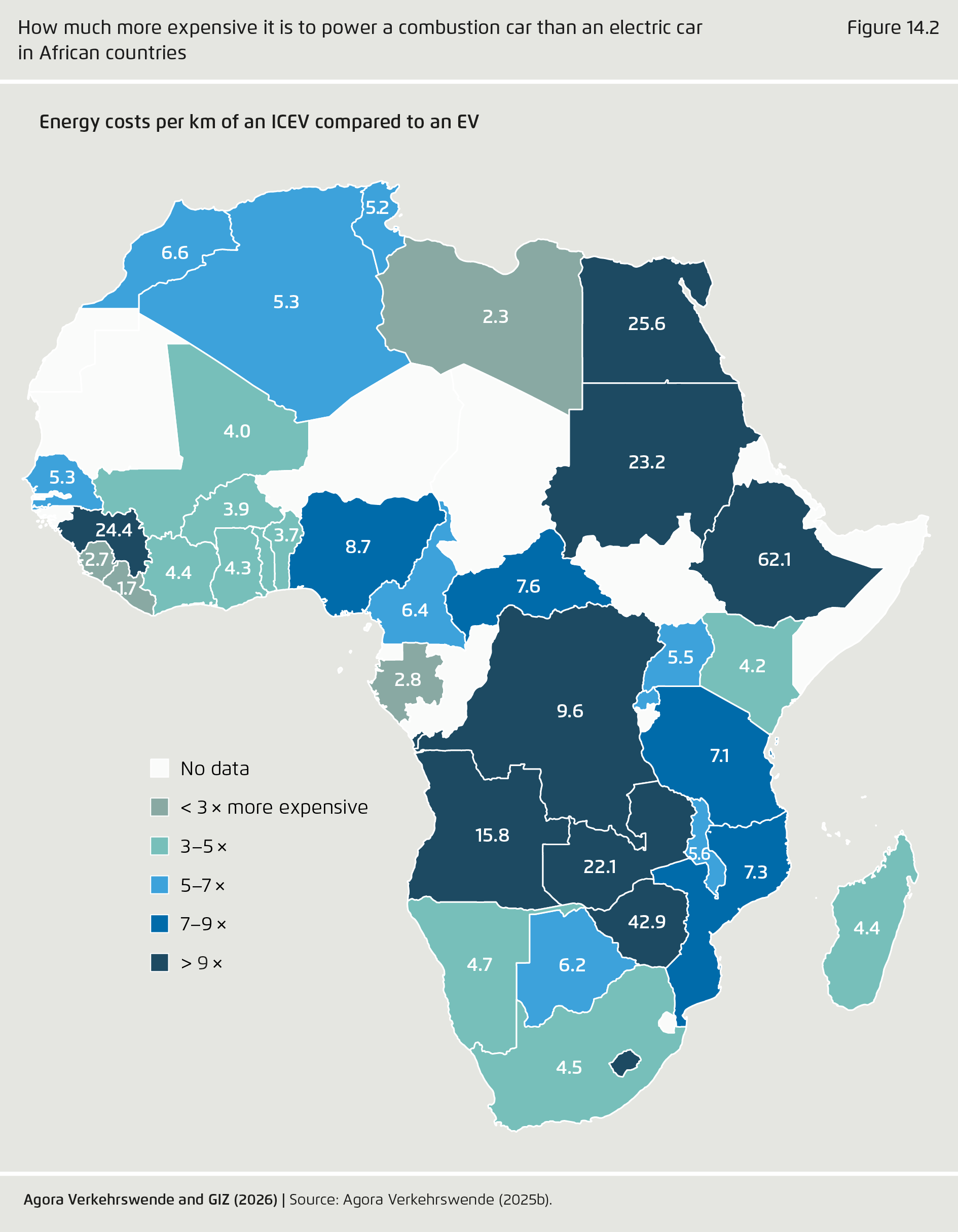

Africa’s abundant renewable energy and mineral resources provide a solid basis for transitioning transport away from imported fuels towards electric and sustainable mobility. In most African countries, petrol vehicles cost around 5.5 times more to operate per kilometre than electric vehicles, reflecting the higher efficiency of EVs and the significant differences in electricity prices. These range from below USD 0.01/kWh in countries such as Egypt, Ethiopia and Libya, to above USD 0.30/kWh in Guinea-Bissau, Comoros and Cape Verde. In contrast, fuel prices vary less in other countries, ranging from below USD 0.40/l in Angola, Algeria and Egypt to above USD 1.50/l in the Central African Republic, Senegal and Zimbabwe. This makes EVs most competitive where electricity is cheap (see Figure 14.2).18 Focussing on electric mobility can reduce costs, increase access and release strain on tight public budgets.

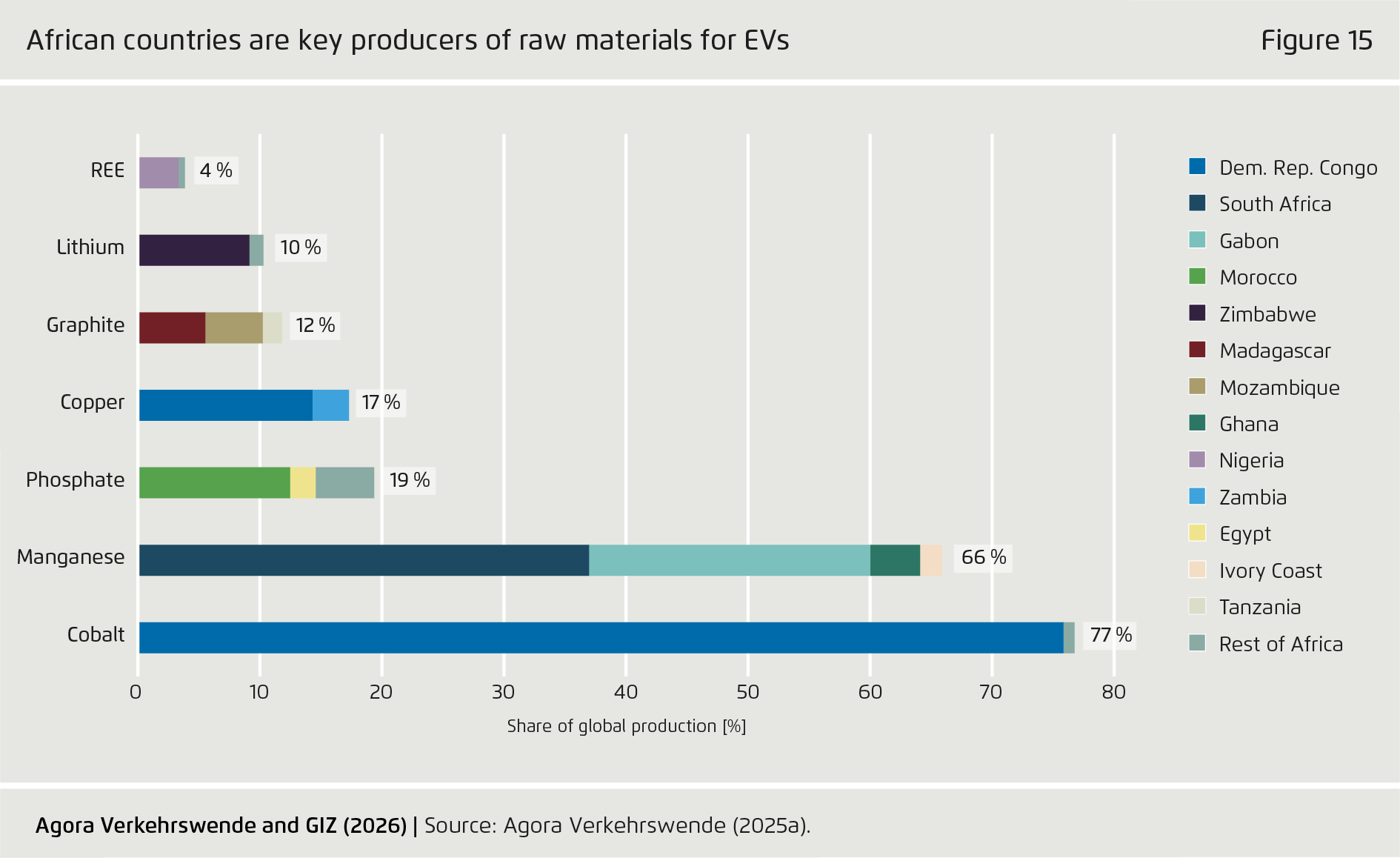

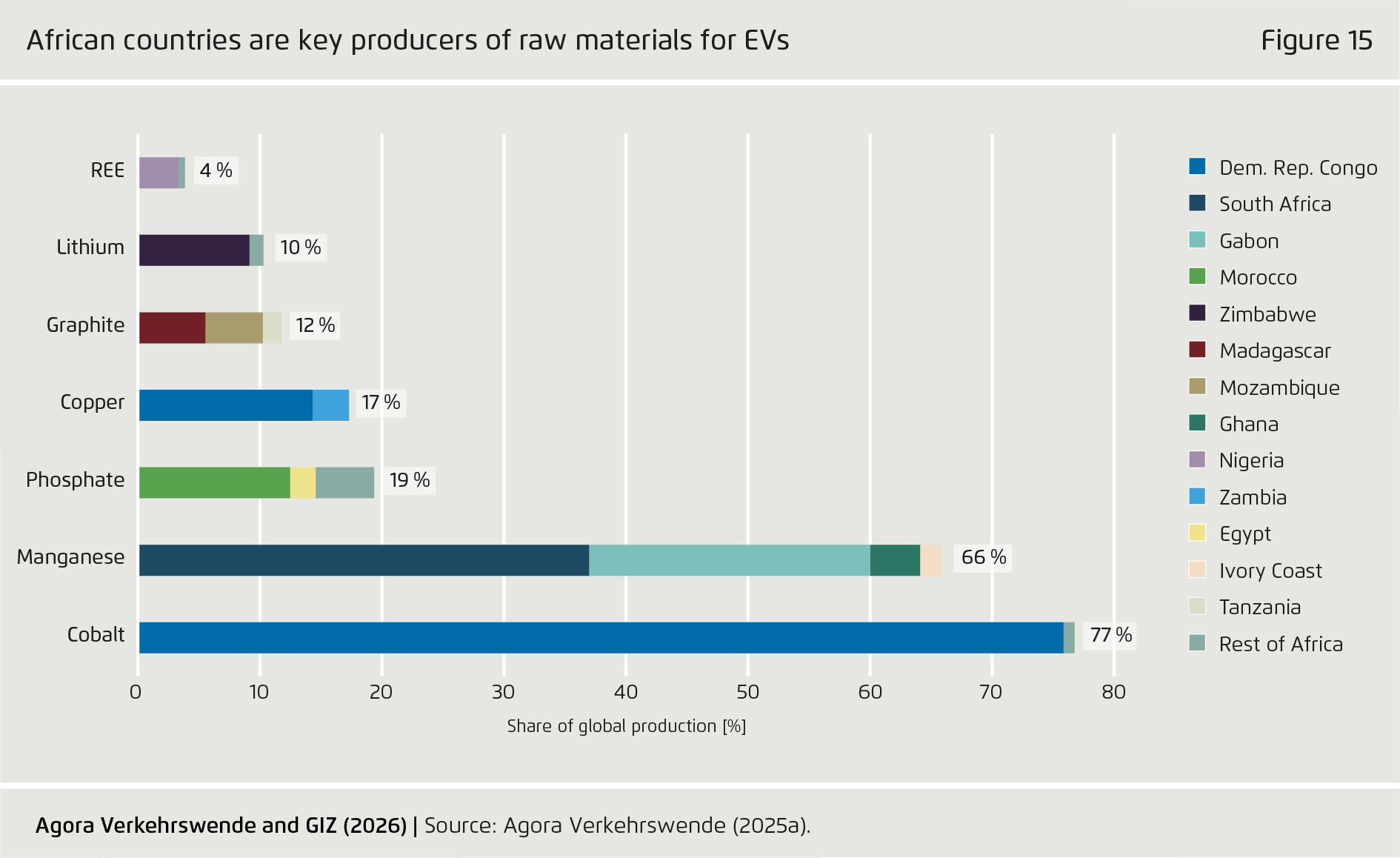

At the same time, Africa is a key player in the global EV supply chain. It dominates manganese production, with South Africa accounting for 37 % of production and Gabon for 23 %. The DRC supplies 74 % of the world’s cobalt and 14 % of its copper, while Morocco provides around 13 % of the world’s phosphate (see Figure 15).19 This creates growing opportunities for the continent’s economy, particularly if more of the raw materials can be processed within Africa.

African governments are increasingly adopting ‘produce locally, sell locally’ strategies, making significant investments in basic assembly to move away from importing used vehicles as a first step towards full domestic manufacturing. Various measures, including the bans on used vehicle imports introduced in countries such as Egypt and South Africa, have supported this shift.

Meanwhile, countries such as Algeria, Ethiopia, Ghana, Kenya, Nigeria and Rwanda are increasing local production by setting up Semi-Knocked Down and Complete Knocked Down vehicle assembly plants. Uganda’s state-owned Kiira Motors has been producing electric vehicles since 2011, and BasiGo in Kenya has established an assembly facility with the capacity to produce up to 30 electric buses per year. At the same time, major manufacturers such as BYD and Ford are entering the market with plans to set up local assembly plants. The East African region is emerging as a hub for the assembly of electric vehicles (EVs), including two- and three-wheelers, buses, and passenger cars.

3.4 Ambition and action on electrification are increasing

In developing countries and emerging economies, the NDC process plays a key role for demonstrating national climate ambitions and for attracting international financial and technical support. In their latest NDCs, African countries have identified electric mobility as a key means of achieving climate-neutral transport and mobility.

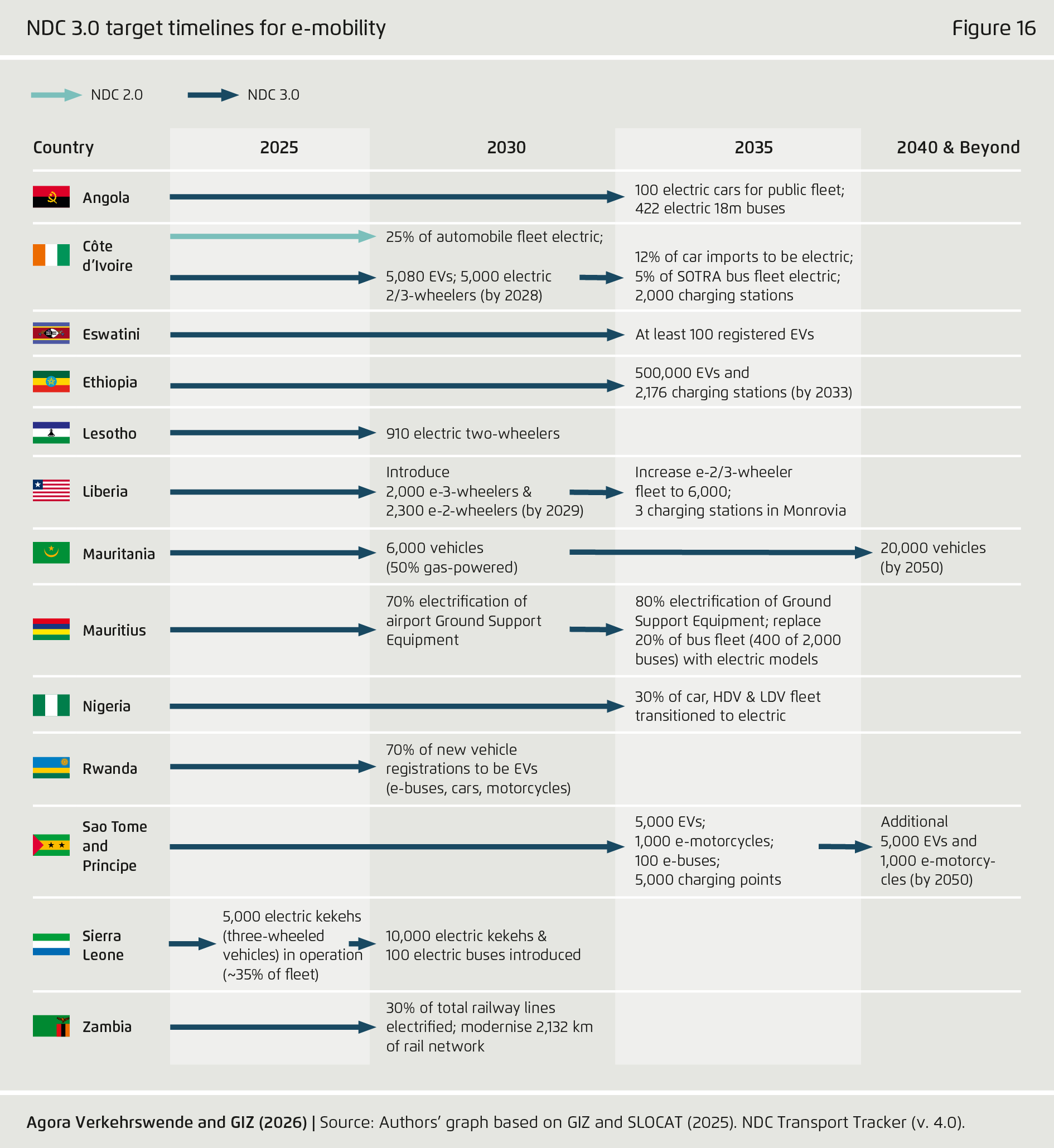

African nations comprised 26 of the 102 countries that had submitted third-round Nationally Determined Contributions (NDCs) by mid-December 2025. Among submissions from African nations, 13 contain targets for the expansion of electric mobility. This represents a significant step forward by African countries in formal climate planning, as the vast majority of African NDCs that contain EV commitments exhibit ambition that was absent from the previous round of submissions. This indicates a decisive shift from general intentions to concrete, sector-specific strategies (see Figure 15).

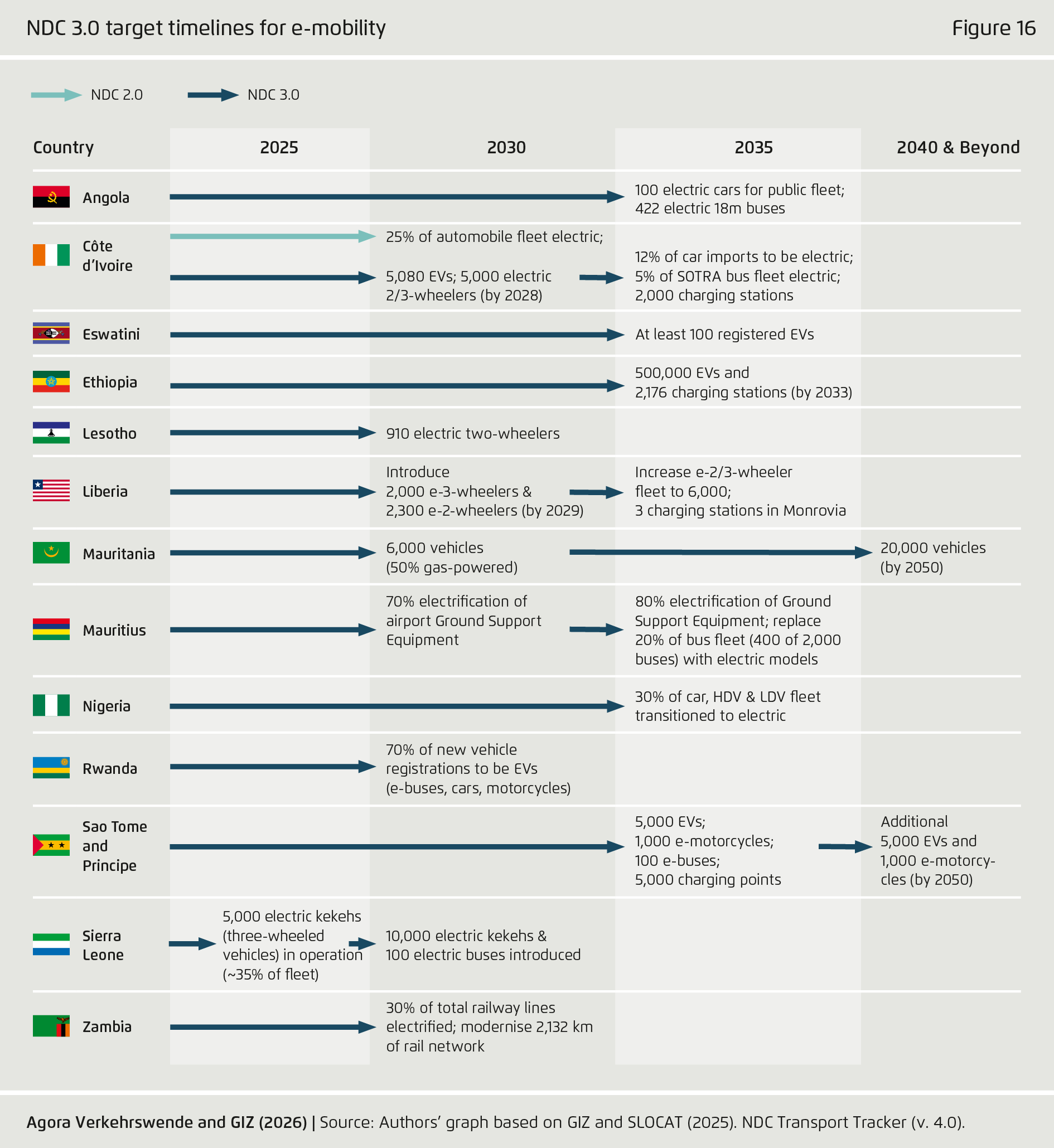

The pledges from African nations vary in scope and scale, reflecting diverse national priorities. Rwanda has set one of the continent’s most ambitious market-share targets, aiming for 70 % of newly registered buses, cars, and motorcycles to be electric by 2035. In West Africa, Sierra Leone, Côte d‘Ivoire and Liberia are focusing on high-impact segments: Sierra Leone is seeking to deploy 10,000 electric three-wheelers (‘kekehs’) and 100 electric buses; Côte d‘Ivoire is aiming for 5,000 electric two- and three-wheelers and a 12 % share of electric car imports; and Liberia foresees adoption of 6,000 electric two- and three-wheelers. Ethiopia stands out for the ambition of its plan to roll out 500,000 electric vehicles by 2033, complemented by a specific plan for over 2,000 charging stations. Other nations, such as Angola, Mauritius, and Nigeria, are prioritising public and commercial fleets, with targets for hundreds of electric buses or specific percentages for electrifying government vehicles.

This mosaic of commitments demonstrates a clear continent-wide recognition of e-mobility’s role in development and decarbonisation, albeit with strategies tailored to local transport ecosystems and economic capacities.

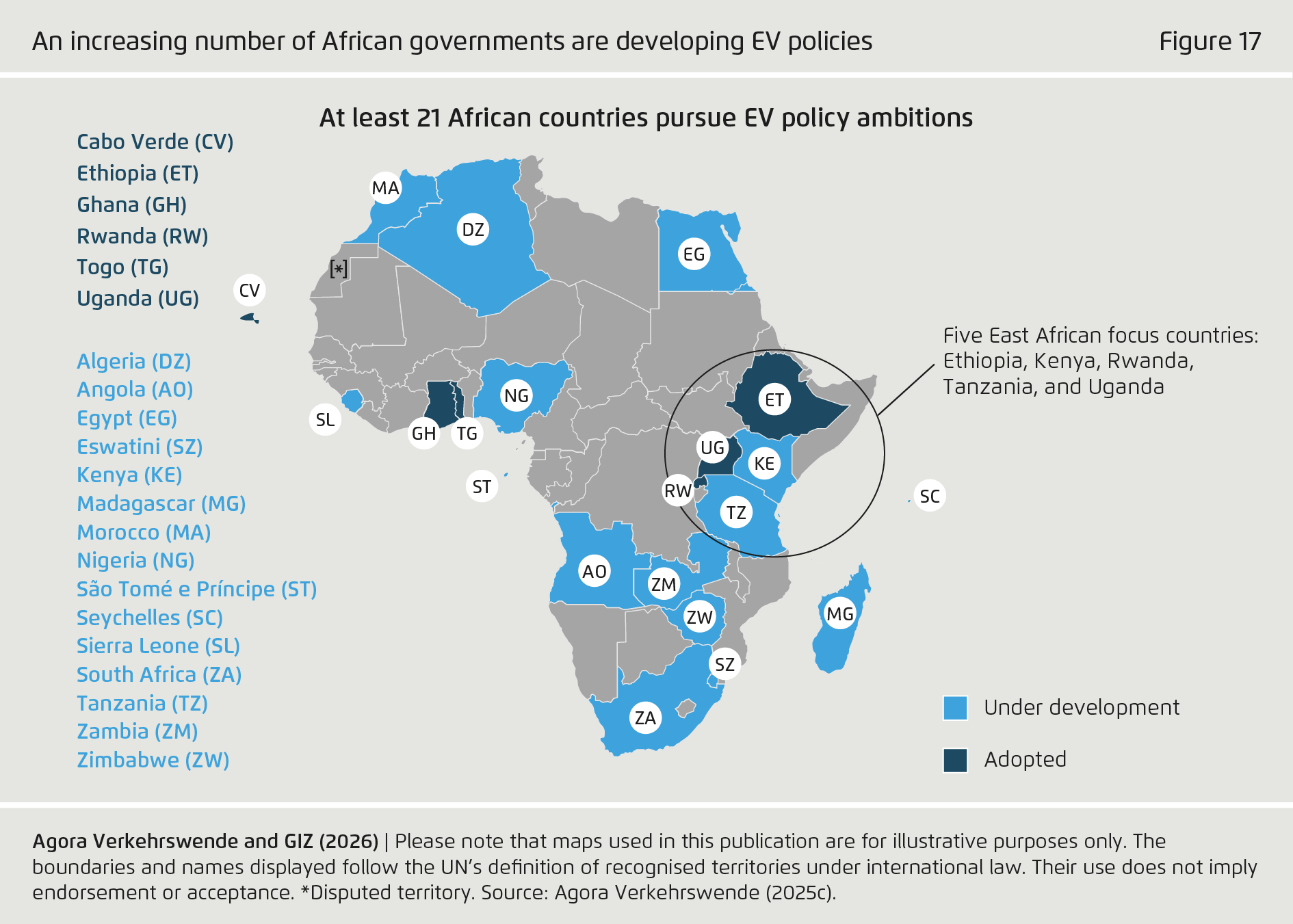

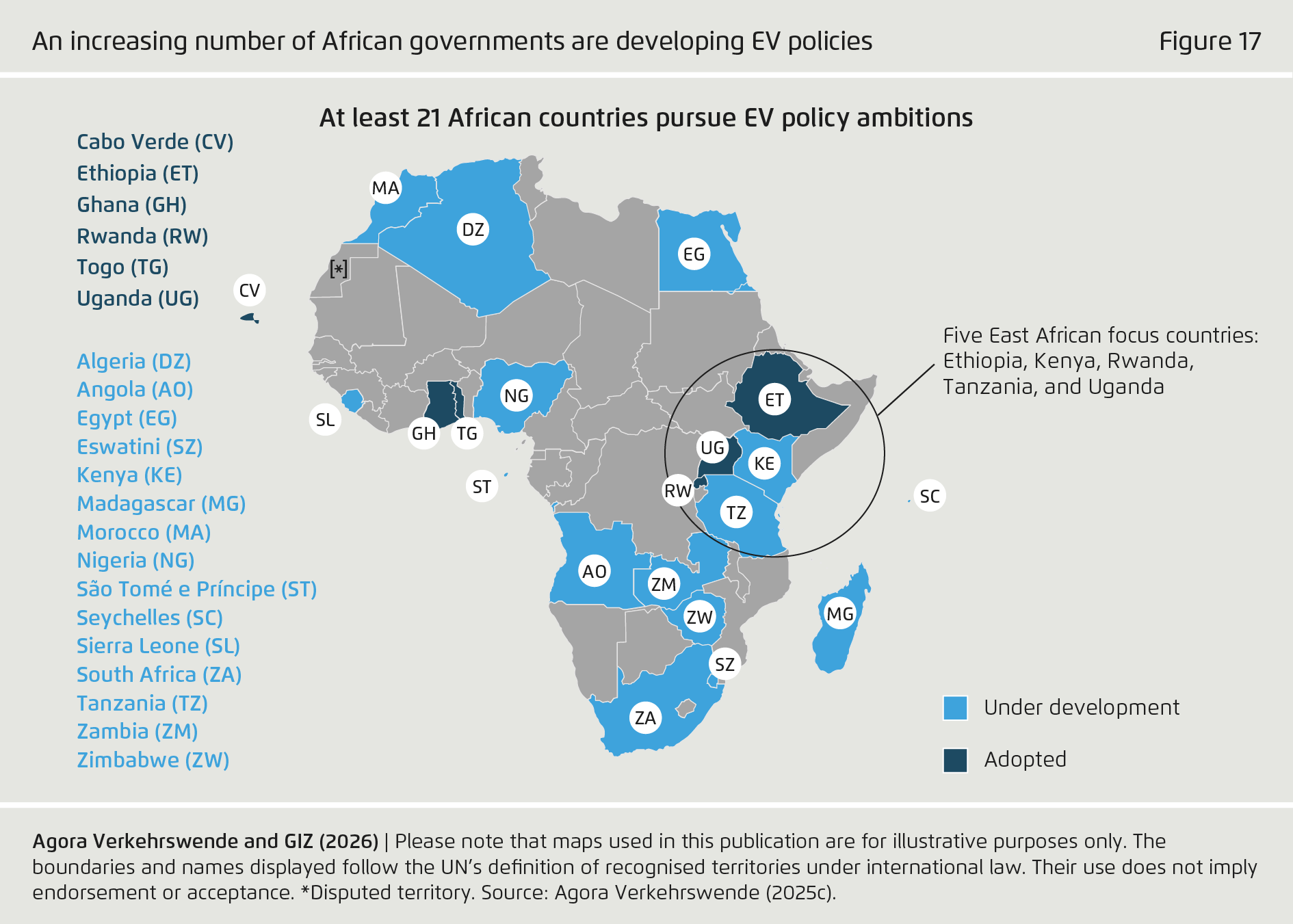

All NDCs submitted by African nations acknowledge the importance of e-mobility, and at least 21 African nations have adopted specific strategies to accelerate the uptake of electric vehicles, using a variety of policy instruments.East Africa is a leading region for the adoption of electric mobility, with Ethiopia, Kenya, Rwanda, Tanzania and Uganda emerging as the continent’s frontrunners. Figure 16 shows the countries that have already adopted or are currently developing national EV policies or strategies.20 Other large national markets, including Ethiopia, Morocco, and South Africa, have seen rising EV sales, although data remain limited and national definitions vary. There is growing momentum for EV adoption in Africa. However, ambition and progress remain uneven, with policies in many countries still in the development phase.

The energy sector plays an extremely important role for the adoption of EVs, as it determines the availability of charging infrastructure (a crucial factor for ease of use) as well as the price differential between electricity and combustion fuels (a crucial factor for EV cost competitiveness). In this regard, African countries are well positioned, as most have substantial renewable energy potential. For example, Ethiopia, Kenya and the Democratic Republic of Congo already generate over 90 % of their power from renewables.21 By adopting comprehensive EV policy frameworks and strengthening cooperation, African countries can leverage economies of scale to develop a robust regional EV market.

Accelerating and scaling early progress in electric mobility will require long-term policy certainty and enhanced coordination among African countries. Therefore, coordinated action across the domains of policy design, standardisation, infrastructure deployment and market development is essential to building a resilient, scalable regional electric vehicle (EV) ecosystem.

4 | Conclusion

Delayed action will necessitate higher future costs

Transport emissions in the G20 grew just under 4 % between 2015 and 2024, which is much lower than that of past decades. Furthermore, many G20 nations have made significant progress in adopting policy to bring about a climate neutral transport sector, as evidenced in part by the slow decoupling of economic growth from transport emissions. However, far greater ambition is required to fulfil the objectives of the Paris Agreement. Time is running out to achieve the deep emission cuts that are required. The transport sector is traditionally slow to change; lack of progress today will mean a shrinking window for action that will force a more costly transition in the future.

Advances in the energy transition mask shortfalls in changing mobility patterns

Over the last decade, many G20 countries have taken steps towards the electrification of road transport by setting objectives for electric vehicle (EV) penetration, sales and charging infrastructure, albeit with varying degrees of ambition. In many cases, these targets are supported by specific policies. While the market for EVs and other zero-emission vehicle technologies was virtually non-existent in 2015, EVs are now a common sight on the road in many countries. Global EV car sales reached a 22 % market share in 2024, compared to just 0.7 % in 2015. Of the 39 million electric cars worldwide, 96 % are on the roads of G20 countries. However, national adoption is proceeding at different speeds.

Despite this progress, alternative vehicle technologies will not be sufficient to fully decarbonise the transport sector against the backdrop of rapid population growth, rising motorisation rates and the trend towards larger vehicles. More efficient transport systems are therefore essential for transport system decarbonisation. Measures that support a shift towards more efficient, less carbon-intensive modes of transport are still too scarce. While all countries are investing in public transport infrastructure, this investment often fails to keep pace with rising demand, much less induce the additional demand required for a modal shift. Greater efforts are needed to develop new mobility services and boost the appeal of public transport, active mobility, and low-carbon freight alternatives.

Vehicle efficiency standards and electrification measures should be complemented by measures to reduce vehicle weight

One factor undermining efforts to improve the energy efficiency of vehicles is the increasing popularity of larger, heavier vehicles. EVs are no exception to this trend. To ensure that envisaged carbon reductions are achieved, measures should be taken to encourage the use of smaller, lighter vehicles. Additionally, smart vehicle design – including advanced aerodynamics, lightweight materials, and intelligent powertrain systems – can greatly enhance vehicle efficiency. In the case of EVs, this minimises additional demand for electricity, thus reducing costs for grid and generation-capacity expansion.

Measures that reduce transport demand without compromising mobility are needed

The COVID-19 pandemic gave new impetus to rethinking individual transport behaviour and has led to new work patterns, allowing for more work from home and less business-related travel. Modern communication technologies are an important catalyst for change in this area because they enable alternatives to travel, such as video conferencing. It is important to maintain this momentum and explore further improvements that can reduce travel without hindering mobility needs. Modern technologies can optimise freight routes and loads, reduce travel distances and increase load factors. Optimised traffic routing, supported by adaptive technology, can improve overall traffic flow and reduce travel and idling times.

It is important to remember, however, that harnessing the power of information technology to lower transport demand necessitates broad access to reliable, high-speed communication infrastructure. In addition, urban planning that ensures basic services are close to home is an important means of reducing transport demand.

Fossil-fuel subsidies should be eliminated

Although many countries had started to reduce fossil fuel subsidies, as shown in the dashboard, support for fossil fuel transport soared in many G20 countries in 2022 due to rising energy prices as a consequence of the Russian invasion of Ukraine. Although subsidy levels in the G20 fell in 2023, overall subsidy levels continue to distort the market by giving carbon-intensive modes of transport an unfair advantage.

Revenues spent or forfeited to finance fossil-fuel subsidies could instead be used to enhance the availability and cost competitiveness of public transport and to support both the electrification of vehicles and the market uptake of electricity-based zero carbon fuels for aviation and shipping. Eliminating effects that distort the price of fossil fuels would also support a higher share of renewables in the power mix. A shift towards fully renewable power generation would help to reduce GHG emissions in the power sector and support zero-carbon transport options. It would also reduce local air pollution, which is an important reason for many countries to pursue electrification.

G20 activities should reflect the need for integrated system approaches

Many of the necessary developments in the transport sector, such as electrification and digitalisation, require close integration with other sectors. The organisational structure of G20 working groups and task forces should reflect this fact. To date, the G20 has yet to establish a work stream dedicated to transforming transport. By pooling the expertise of IT, transport, and power grid experts, it should be possible to identify measures that can promote greater integration between the power and transport sectors, and, by extension, guide the decarbonisation of the transport sector and the energy economy as a whole.

1 Argentina, Australia, Brazil, Canada, China, France, Germany, India, Indonesia, Italy, Japan, Mexico, Russia, Saudi Arabia, South Africa, South Korea, Turkey, the United Kingdom, the United States and the European Union.

2 Data only available until 2022.

3 Low-carbon power generation includes renewables and nuclear power.

4 The final coal-fired power plant was taken offline in September 2024.

5 UN (no date); World Bank (no date).

6 European Commission (2025).

7 Agora Verkehrswende and GIZ (2023).

8 Johansson and Mutiso (2025).

9 Agora Verkehrswende and GIZ (2023).

10 Agora Verkehrswende and GIZ (2023).

11 ITDP and UC Davis (2024).

12 Tam (2024).

13 AREMI (2024).

14 GreenCape (2025).

15 Knoope and Terwindt (2023).

16 SLOCAT (2023).

17 Agora Verkehrswende (2025b).

18 Agora Verkehrswende (2025b).

19 Agora Verkehrswende (2025a).

20 Agora Verkehrswende (2025c).

21 IEA (2022).

Bibliographical data

Further reading

Downloads

-

Study

pdf 8 MB

Towards Decarbonising Transport 2026

A Stocktake on Sectoral Ambition in the G20

All figures in this publication

GDP (PPP, in constant 2021 international dollars) and population by region, 2015, 2024 and 2050

Figure 1 from Towards Decarbonising Transport 2026 on page 5

Share:

Distribution of GDP (PPP, constant 2021 international dollars) within the G20 of G7, BRICS+ and other members, 2015 and 2024

Figure 2 from Towards Decarbonising Transport 2026 on page 6

Share: